English

Follow us

on Twitter

@Bank_CIC

Dear Clients,

The speculator George Soros, who became famous for betting against the pound sterling, once railed against Germany: “Because of its history, Germany fears inflation more than recession. For the rest of the world, it is exactly the other way round.” He wouldn’t say the same thing today. In the current situation, with prices going up, nearly all central banks are being forced to raise their benchmark interest rates to combat inflation. Now they seem to be acting almost out of panic, but as recently as last autumn they were still calling the price rises a temporary phenomenon. The move towards onshoring some of the key stages of manufacturing crucial to the domestic economy, which has partly been triggered by problems in the supply chain, may potentially result in structurally higher basic inflation. For inflation to run out of control, though, commodity prices would have to move sustainably higher. This is normally associated with a booming economy, which is not what we are expecting under current circumstances. Hence, basis effects are likely to bring considerable relief on the inflation front in the near future.

Mario Geniale

Mario GenialeChief Investment Officer

Economic prospects

No sooner has the dust settled on the Covid-19 pandemic, which laid bare the fragility in manufacturing processes, than another pressing problem is rearing its head. Price increases driven by pent up demand for goods are rapidly picking up pace again as a result of the Ukraine conflict. Both of the warring parties, Russia and Ukraine, are exporters of oil, gas and grain. While Russia is subject to a stifling export embargo, Ukraine – the theatre of war – is having to cope with crop failures and logistical challenges.

Monetary policy inertia and anti-cyclical action

This is having far-reaching financial consequences. The World Bank has cut its global economic growth forecast for 2022 to 2.9%, and the forecast for Russia to -8.9%, pointing to the strict Covid-19 policy in China and worsening financial conditions, as well as energy and commodity-driven inflation. Central banks are now beginning to raise interest rates, albeit a year too late, and drastically restricting the financial options available for fiscal and monetary policy. This is weighing on consumer sentiment and setting off a spiral of macroeconomic implications for the labour market.

With the onerous effects resulting from global inflation having reached 7.8% in April, policymakers have their backs to the wall. A recession can be averted by taking anti-cyclical action at the national level and rigorously eliminating structural inefficiencies in spending policy. This also means taking advantage of the economic recovery to make provisions for future downturns and increase government revenue. This forward-looking approach, which politicians could adopt when trying to woo voters, is already being taken in the corporate world: “cradle to cradle”. (goste)

Markets

The moment of truth is approaching

Companies will be reporting half-year results from mid-July onwards. It will then become clear how much of an impact supply chain problems, high commodity prices, rising interest rates and a shortage of skilled workers are having on corporate profit margins. Financial analysts have not yet revised their earnings estimates. This could put the financial markets to the test once again. The fact that central banks have begun to normalise monetary policy, effectively removing liquidity from the financial markets, is another reason to expect substantial price volatility.

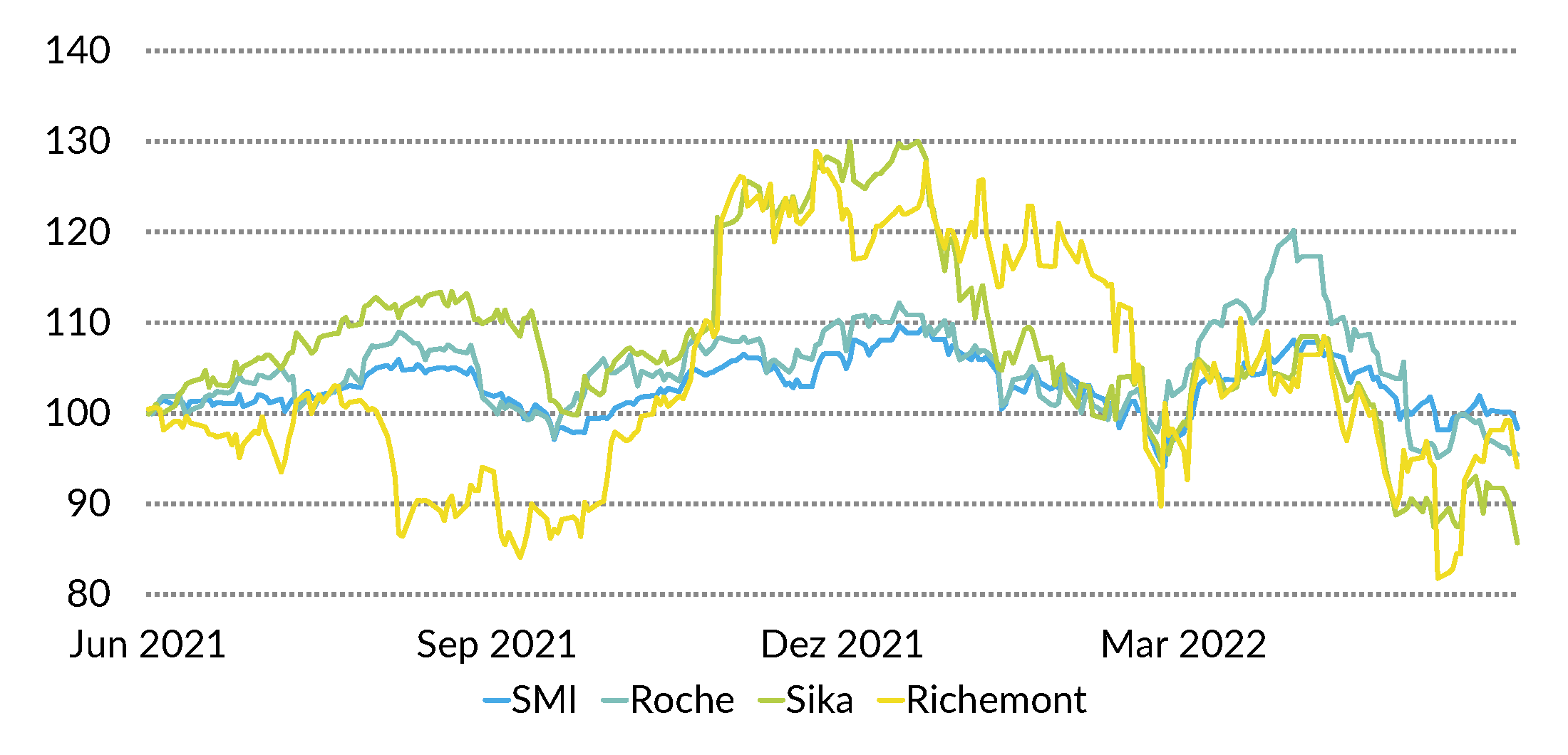

Equities Switzerland

The greater forecasting reliability for the earnings growth of index heavyweights Roche, Novartis and Nestlé suggests that Swiss equities are likely to do better than other markets over the next few months. The Swiss National Bank will start to raise interest rates again in line with the European Central Bank. In the current environment, it is too optimistic to expect a double-digit rise in corporate profits. We therefore favour quality stocks such as Roche, Sika and Richemont. (bae)

SMI

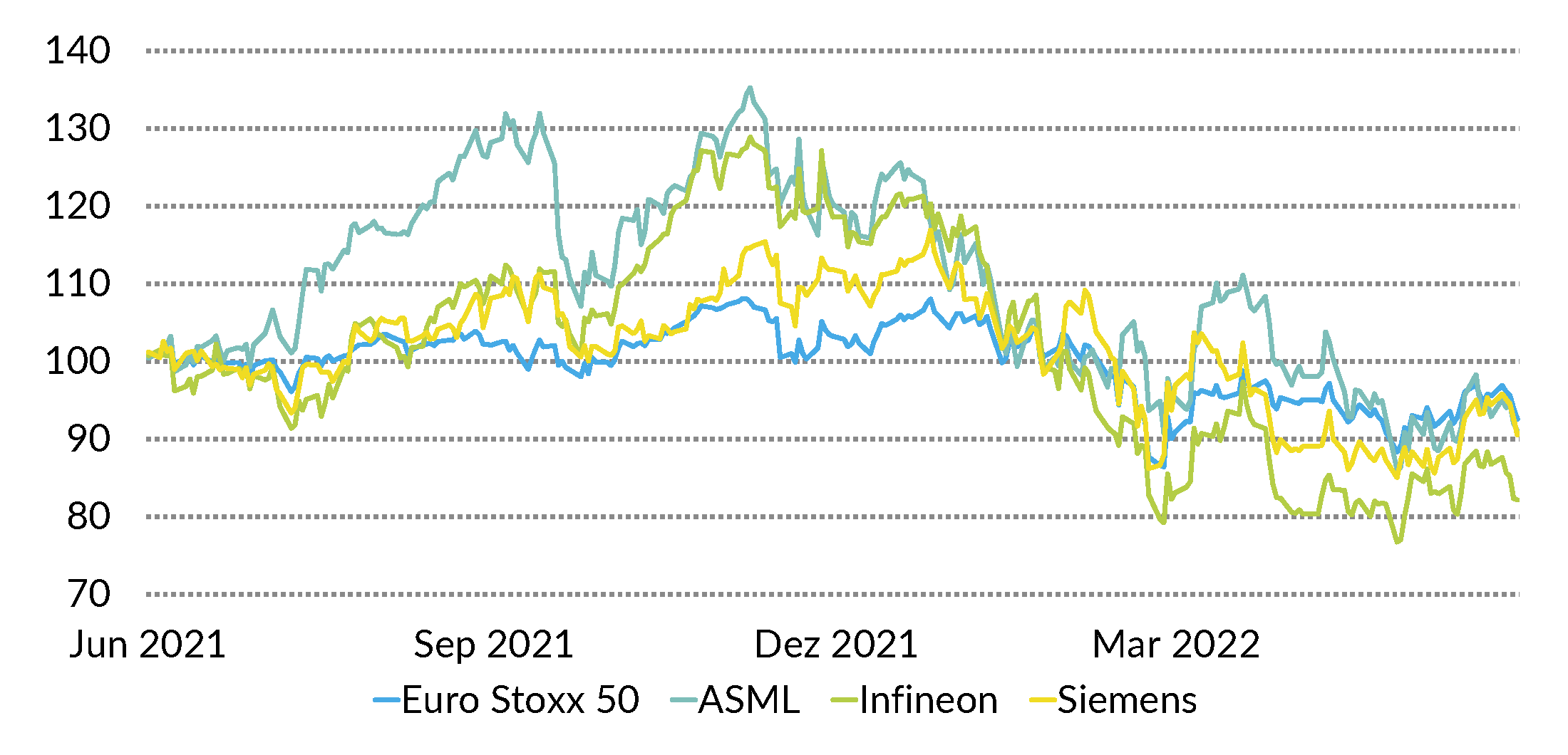

Equities Europe

The war in Europe is affecting a troubled economic area that was already having to cope with Brexit, plans for ensuring a sustainable supply of energy and the scars left by the Covid-19 pandemic. Financial analysts are still holding back on revising their models for future corporate profits, leaving the market looking cheap. The ECB is noticing the inflationary pressure and the cries of protest from savers are becoming louder and louder. A difficult environment which calls for solid investments: ASML, Siemens and SAP. (goste)

Euro Stoxx 50

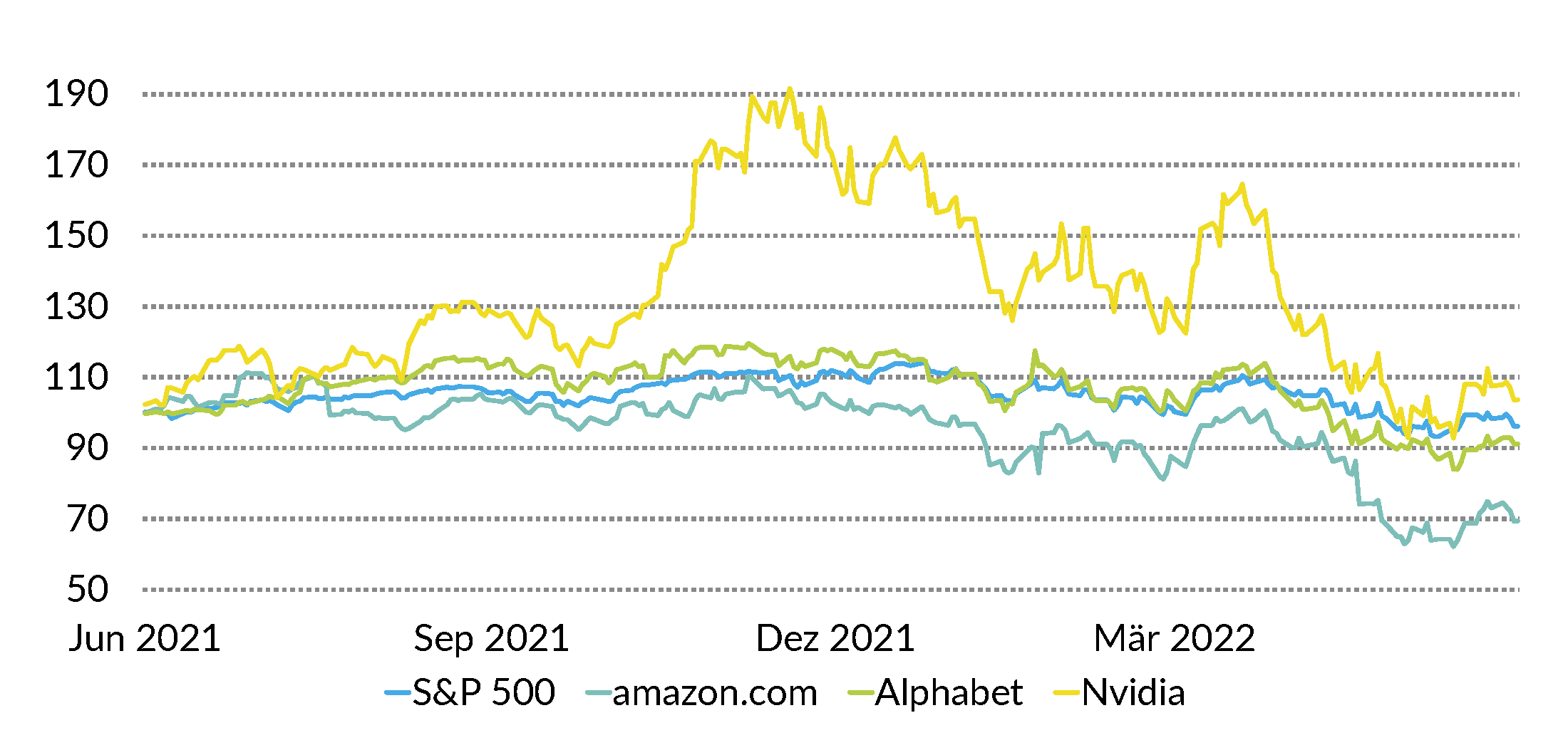

Equities US

Many of the major tech stocks, the winners of the past few years, are continuing to come under selling pressure. Economic growth is constantly being revised downwards by analysts, although estimates of profit growth in the market remain at almost 10%. In the current environment, this seems very optimistic. It is therefore possible that these estimates will need to be adjusted. However, the immense monetary reserves held by the tech giants built up over recent years are waiting for good investment opportunities and should not be forgotten. We favour Amazon.com, Alphabet und Nvidia. (amm)

S&P 500

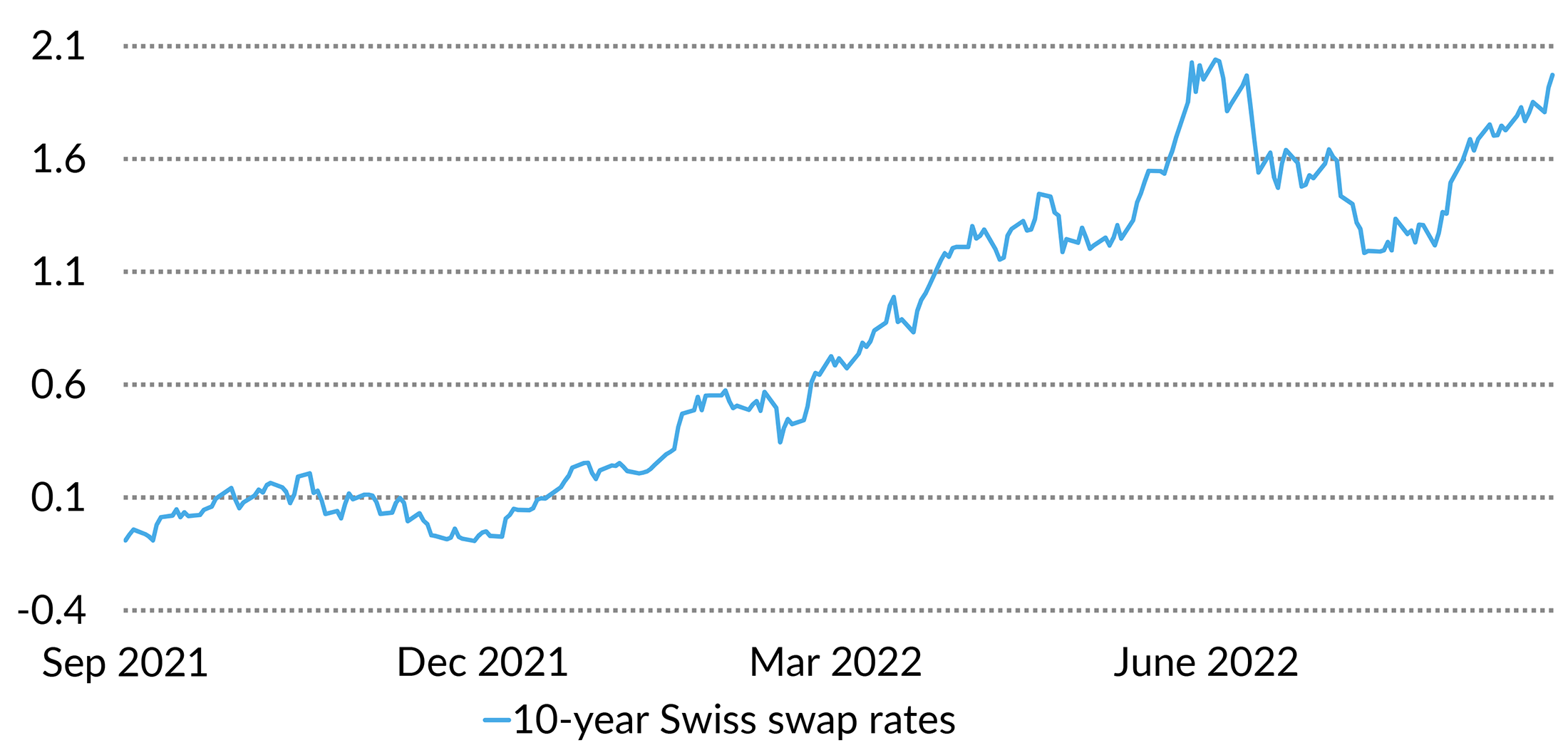

Bonds

The more restrictive policy now being pursued again by central banks to fight escalating inflation has led to uncertainty in the bond markets. The increase in credit spreads at the same time has put additional pressure on bonds. However, we think it is unlikely that there will be another significant rise in yields in the next few months, as we believe inflation has peaked. We continue to favour short-term corporate bonds. (muc)

10-year Swiss swap rates

![]()

Imprint

Editor:

Bank CIC (Switzerland) Ltd.

Marktplatz 13, P.O. Box

4001 Basel, Switzerland

T +41 61 264 12 00

Authors:

Marc Ammann (amm), Roger Baumann (bae), Mario Geniale (mge), Sten Götte (goste), Carl Münzer (muc), Nicolas Laporte (lanic)

Editorial deadline: 30 June 2022