English

Follow us

on Twitter

@Bank_CIC

Dear Clients,

The turn of the year is always a good time for taking stock of the past year and setting goals for the new one ahead. 2022 was a challenging time. The conflict in Ukraine and subsequent economic developments cast gloom over the picture. Consumer price rises reached a level not seen in 50 years. Both equities and bonds posted a negative performance.

You could say that the three big Ds which have emerged in recent years are now truly a part of reality: demographics, deglobalisation and decarbonisation are all issues that have shot up in importance. They will be with us in an even more conspicuous form in the years to come. The uncertainties arising from the COVID-19 pandemic and the latest geopolitical conflicts have pushed globalisation back considerably. The problem of demographic change in the western world is becoming ever more acute. An ageing population that is putting a burden on the pension system, a shortage of skilled employees and declining tax revenues are all problems that need to be fixed. We also cannot overlook the pressing threat from climate change, which is driving technological change and investments in this area.

But I remain optimistic. All of these issues offer major opportunities in the medium to long term. Positive messages can already be identified for the short term. Our assumption is that inflation has peaked, central bank rate hikes are slowing and the upcoming dividend season looks set to be very rewarding.

The year just started will bring changes, new challenges and a host of opportunities. Talk to us about them! We are at your side as your partner in all financial issues. In the meantime I wish you a happy, healthy and successful 2023 – a year we feel we can approach with optimism.

Luca Carrozzo

Luca CarrozzoCIO

Economic prospects

It’s a tricky task: over the past few months, the central banks in the major economic blocs of the USA, the European Union and Switzerland have been draining huge amounts of liquidity out of the real economy. Surging inflation – driven by high energy prices, supply chain interruptions as a result of Covid-19, and the war in Ukraine – is forcing the guardians of monetary policy to take resolute action. At the same time, the economy is booming. Switzerland stands out with growth of 0.5%, while growth is also taking off in Europe (2.1%) and the USA (1.8%). But one trend is clear from the figures: compared with the growth figures in the first quarter of 2022, the third-quarter figures show a considerable slowdown.

Disinflation in 2023?

Looking at the details, the interest rate hikes are having an impact across the board. The housing market has been faltering since as long ago as the start of the year. Sentiment among managers is becoming increasingly gloomy and consumer demand is shifting towards low-ticket items. By hiking rates to 4%, the Fed is choking off the US economy. The question is whether there will be a recession this year. Forecasts of 1.3% for US GDP growth in 2023 suggest a supportive picture, with unemployment expected to reach 4.4% (currently 3.7%). Inflation should slow to 2%, driving real interest rates (the interest rate minus inflation) to 2%. Apart from bond holders, i.e. creditors, no one enjoys rising real interest rates – certainly not the USA, which is highly indebted. Financial markets deal in expectations, and rising unemployment as inflation is easing could trigger hopes of rate cuts in the second half of the year. This is likely to support the economy and equity markets.(goste)

Markets

Equity markets remain volatile

The first quarter of 2023 looks set to be marked by uncertainty in various respects. The upward pressure on inflation is likely to fade as a result of the base effect. If inflation has peaked, central banks will turn their attention back to economic performance. This being so, benchmark rates will probably peak in the first quarter of 2023. On the other hand, corporate margins will come under pressure. We recommend focusing on quality stocks and a balanced sector allocation.

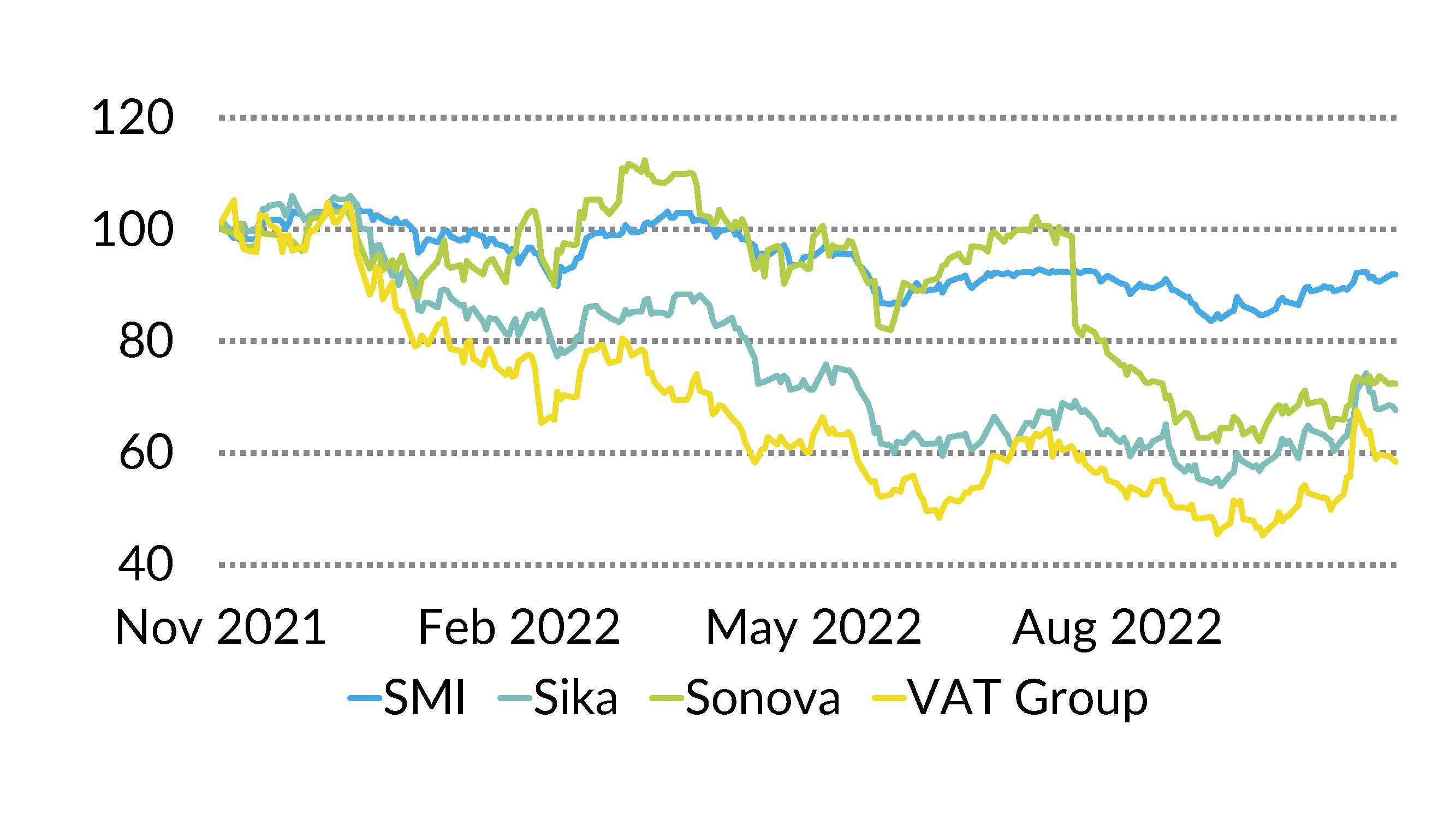

Equities Switzerland

Even though the Swiss equity market is seen as defensive owing to the high weighting of Roche, Novartis and Nestle, Swiss stocks underperformed the European average in 2022. This is a result of the strong franc, which has an negative impact on company profits. But many Swiss companies are market leaders in their field and have pricing power. Amongst blue chips we favour Roche, Sika and Sono-va; in midcaps Bachem, SIG and VAT Group. (bae)

SMI

Equities Europe

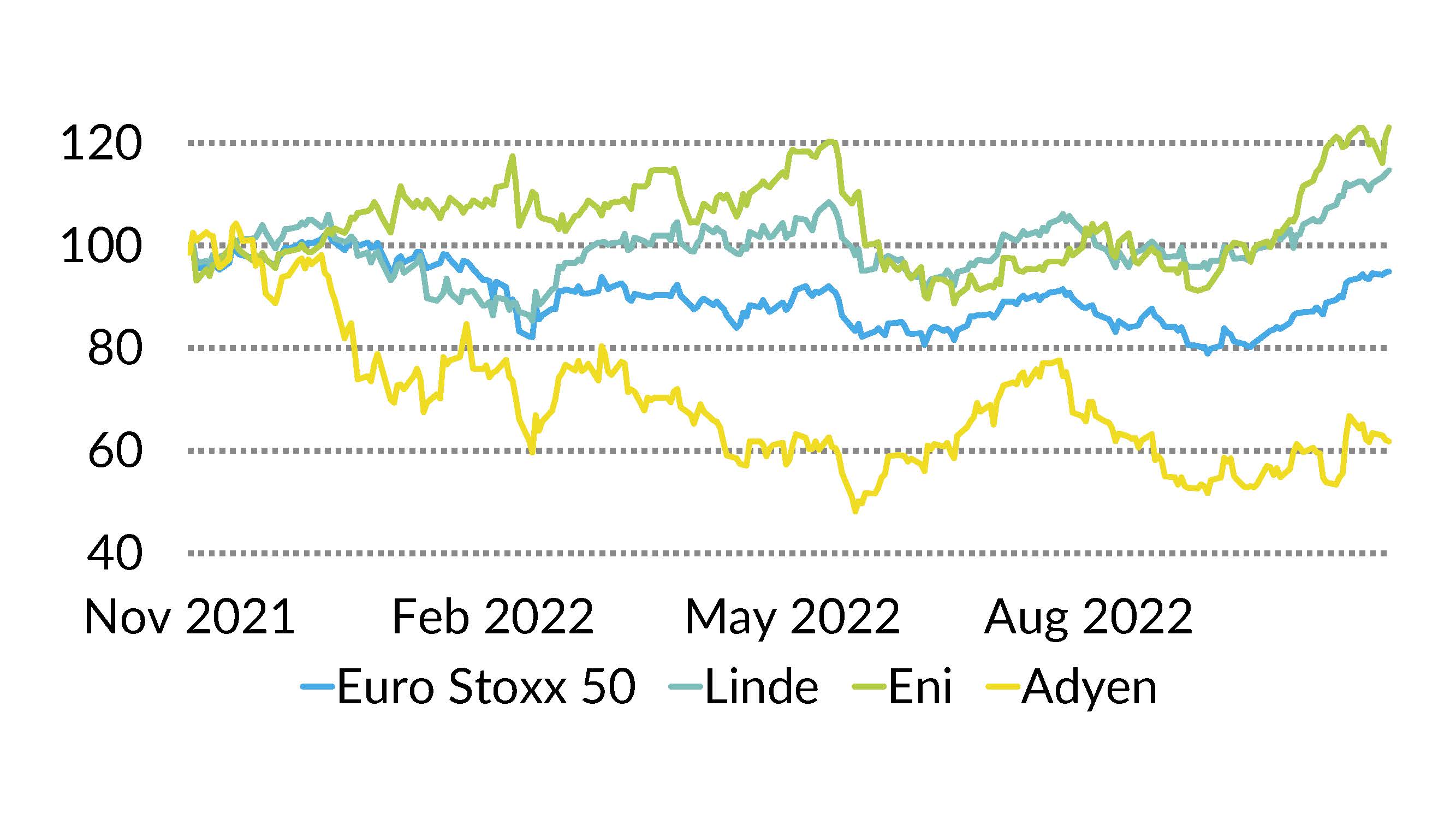

In 2022, the secret winners on the equity market came from Europe. Value stocks with high dividends beat growth stocks, which were hit by inflation and rate hikes. This trend looks set to continue on premiums of over 10% in December, as the ECB is not expected to provide any help. From the middle of the year onwards, these premiums will ease and sentiment will shift to growth stocks such as ASML, Infineon and Adyen. We are aiming for a balanced portfolio: Linde, Eni and Adyen. (goste)

Euro Stoxx 50

Equities US

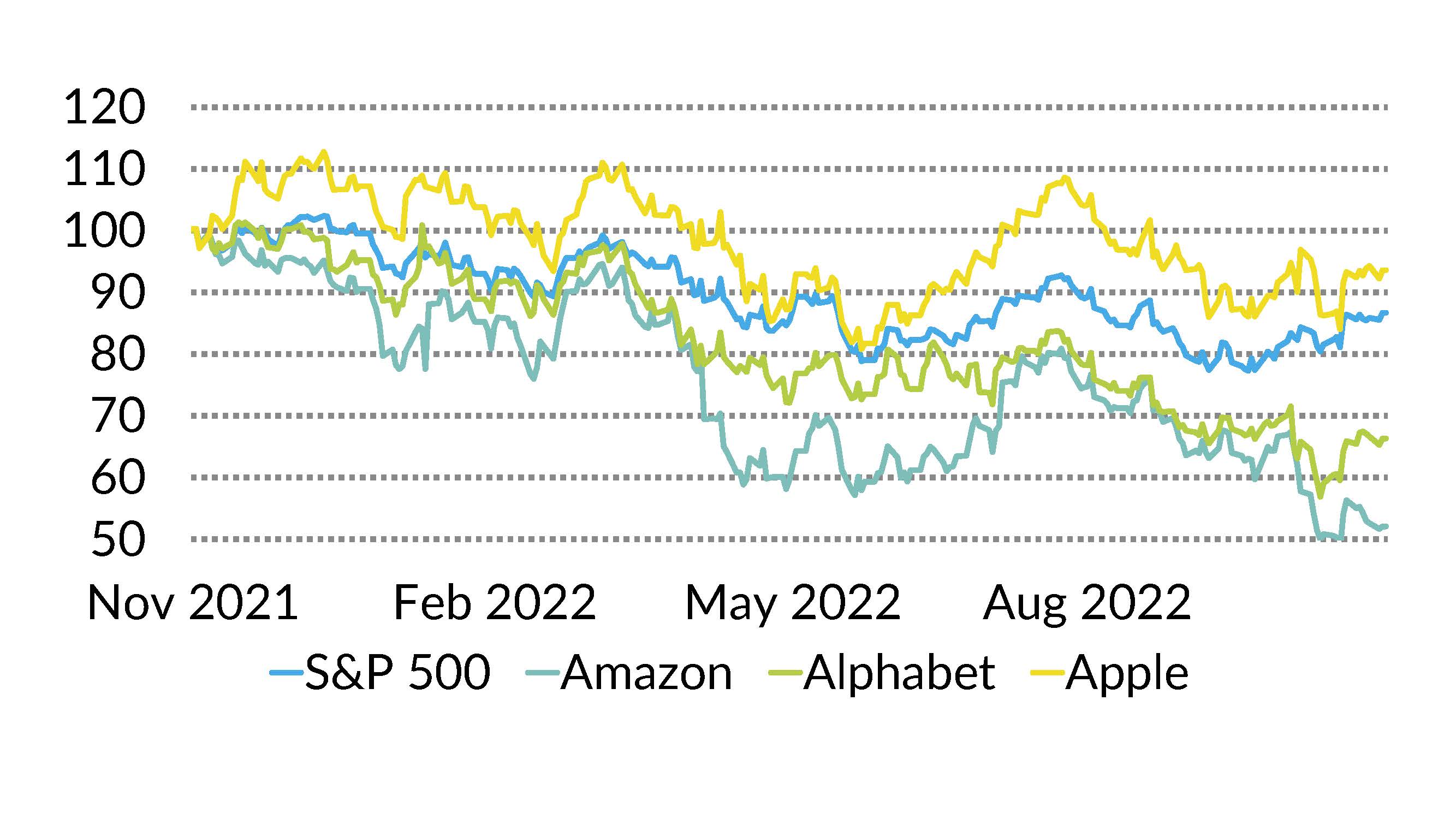

In 2022, the US equity market and investor sentiment suffered under the Fed’s monetary policy actions. On top of this came higher input prices and problems in the supply chain. In many cases, companies will not be able to raise their own prices until 2023. Valuations right now are moderate. The major tech giants are also sitting on billions of dollars in cash – which is now earning a higher interest rate – and waiting for the right investment opportunity. This makes us positive about the US tech sector in particular. We recommend Alphabet, Amazon and Apple. (amm)

S&P 500

Bonds

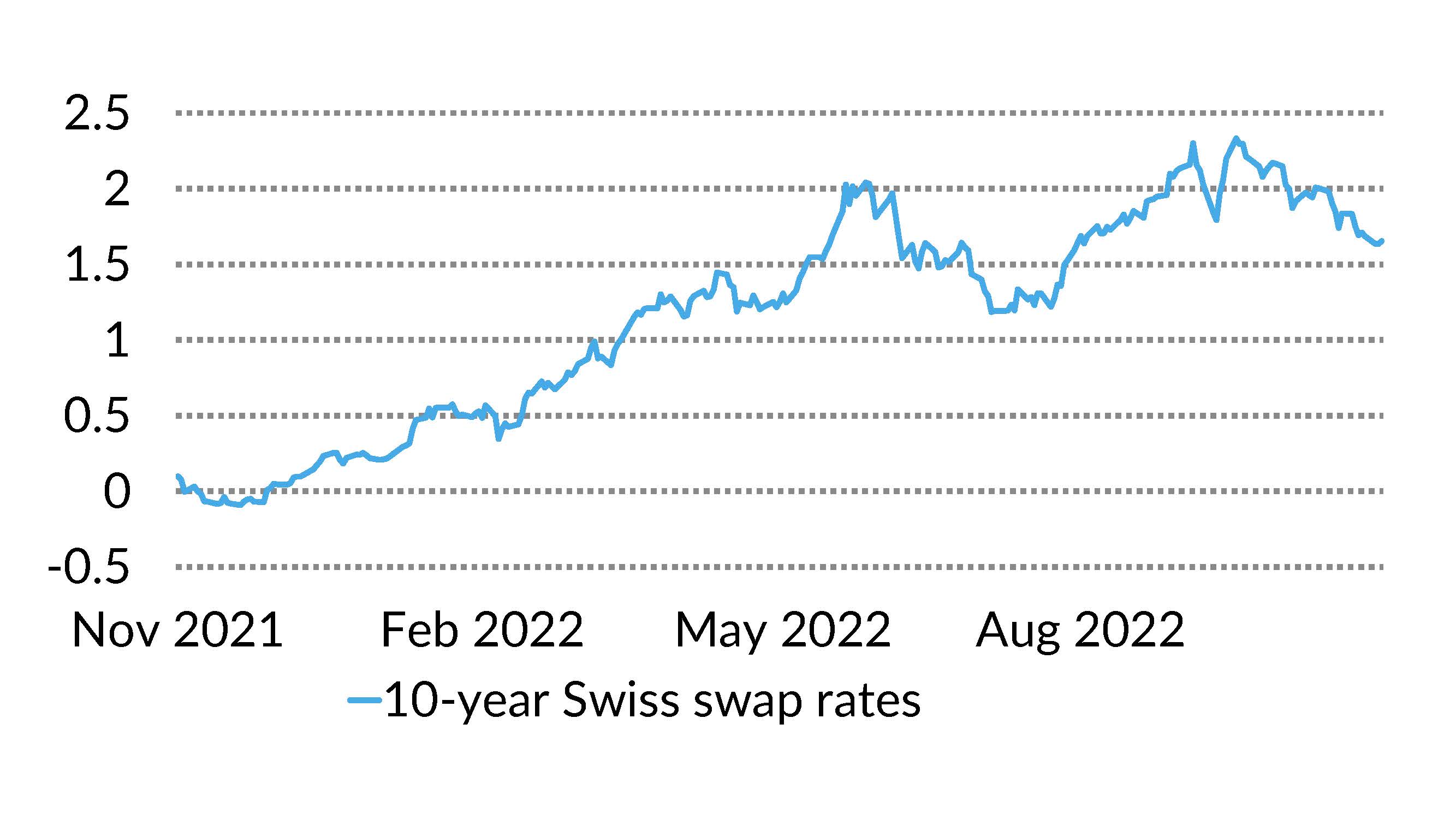

The cycle of central bank tightening should come to an end in the first half of 2023. In an uncertain environment, the return of bond yields and the improved risk/return profile have put the asset class back to centre stage in the minds of investors. The fact that the yield curve in Switzerland is relatively flat, and even inverted in Europe and the United States, suggests investments should be made in shorter maturities. Caution should still be exercised when selecting, but bonds look more attractive than they have done for a long time. (muc)

10-year Swiss swap rates

In brief

Simple and secure cashless payments

The new Visa Debit Card from Bank CIC has arrived! The modern Visa Debit Card enables you to withdraw cash, make cashless purchases and shop online 24 hours a day – in more than 200 countries all over the world.

Advanced functions like mobile payment and independent card management in CIC eLounge make you flexible and self-sufficient. Just like with a Maestro card, your transactions are posted to your account.

It’s easy to order a Visa Debit Card yourself in eLounge or from your personal relationship manager.

Changes to depositor protection

Deposit protection is changing from 1 January 2023 for account balances held at banks. In the event of a bank going bankrupt, CHF 100,000 will be protected and the financing of the system will be strengthened. The new law mainly affects holders of joint accounts. This includes, for example, accounts in the names of spouses, simple partnerships, communities of heirs and condominium associations. Full information on the changes, together with examples, can be found at esisuisse.ch/en/2023.

![]()

Imprint

Editor:

Bank CIC (Switzerland) Ltd.

Marktplatz 13, P.O. Box

4001 Basel, Switzerland

T +41 61 264 12 00

Authors:

Marc Ammann (amm), Roger Baumann (bae), Luca Carrozzo (cal), Sten Götte (goste), Carl Münzer (muc)

Editorial deadline: 16.12.2022