Perspectives 02/2026

Content for residents of Switzerland (see footnote).

If there is one thing the stock exchange does not like, it is uncertainty. And we saw more than enough of that in the last quarter. Geopolitical tensions continue to overshadow events, energy prices are fluctuating wildly and politics is also sending messages that investors cannot ignore.

- 20 April 2026

- Insights

- Author: Luca Carrozzo

- Markets

US President Donald Trump is once again in the international spotlight and bringing new dynamism. Unconventional statements, typical TACO ("Trump always chickens out") climbdowns and obscure political signals are combining with already fragile global relations. This cocktail is moving the markets. The key element here is not so much individual headlines about the Middle East conflict; rather, it is this fundamental question: how stable are the operating conditions underpinning the financial markets?

In parallel with this, energy prices are currently a seismograph for the global situation. Supply concerns stemming from the partial closure of the Strait of Hormuz, strategic interests and structural change are demonstrating how closely economic development and geopolitical reality are intertwined. Companies and investors have to face up to planning certainty being more a wish than a starting position.

Nevertheless, the markets have a remarkable ability to adapt and recover quickly from any weak phases. Between short-term volatility and long-term trends there is always a way for those who are prepared to take a closer look at the situation and avoid knee-jerk reactions.

Maybe that is the main lesson of this quarter: in an increasingly volatile world, prudence is becoming a competitive advantage for investors.

Luca Carrozzo

CIO

Economic prospects

The Swiss economy grew by 0.2% in the final quarter of last year. Growth over 2025 as a whole was below average, totalling 1.4%. The data available thus far for 2026 on Swiss external trade, the business situation and lead indicators hint at a positive start to the year.

Attention shifted to the Middle East at the end of February as events came to a head with the attack on Iran by the United States and Israel. This led to a partial closure of the Strait of Hormuz, which is notably a major energy supply route. As a result, energy prices soared and inflation expectations increased throughout the world. The potential economic consequences depend to a large extent on how long the conflict lasts, the disruption to energy supplies and how energy prices respond to the situation. Central banks reacted with concern, although they still saw no need to take action in March.

Narrow passage, high price

For our baseline scenario we are working on the assumption that the Strait of Hormuz will not be blocked over the longer term and that the consequences for the global economy will remain manageable. However, in the event of a negative scenario where energy prices stay high over the long term and there is lasting instability in the region, the fallout could quickly make itself felt at a number of levels. That is because of the complex global supply chains and the fact that oil is a key component in many manufacturing processes, as well as the fact that major quantities of other commodities are shipped through the narrow waterway.

For example, the freight premiums and insurance costs for shipping goods would remain high, the scarcity and concomitant price increase of fertilisers could cause the cost of basic foodstuffs to rise, and a scarcity of chemicals for the manufacture of plastic would increase the prices of many intermediate products used in industry. This could result in a return of inflationary forces and weaker growth in the initial phase. In the second phase, an acceleration of the transformation of the global energy system or the diversification to other energy suppliers, as well as increased decarbonisation, would be probable. (muc)

Markets

War increases stagflation risk

The further development of the equity markets depends on the duration of the Iran war. The longer the oil price lingers over USD 100 per barrel, the greater the economic fallout. In the short term, we anticipate a continuation of the volatile sideways trend on the stock exchanges. Any market corrections should be taken advantage of consistently to build up quality stocks. Once there is a solution to the Iran conflict, the oil price could fall sharply and the equity markets could resume their upward trend. (bae)

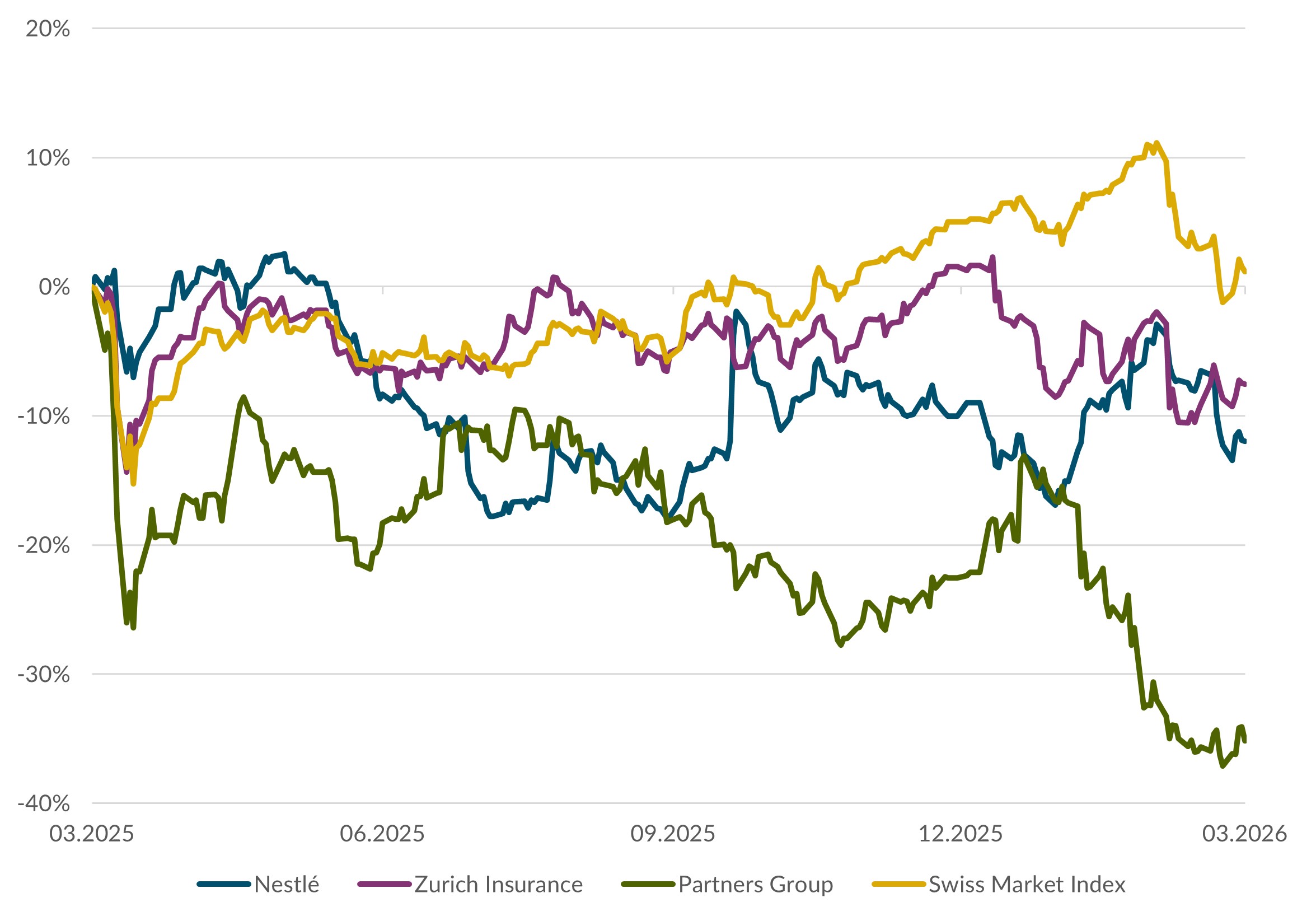

Swiss equities

Negative interest rates are not an option in Switzerland owing to heightened inflation expectations. The Swiss National Bank could purchase foreign currencies instead to prevent a further appreciation of the Swiss franc. The dividend yield on Swiss equities should support the stock exchange at over 3% compared with a mere 0.4% for ten-year Confederation bonds. (bae)

European equities

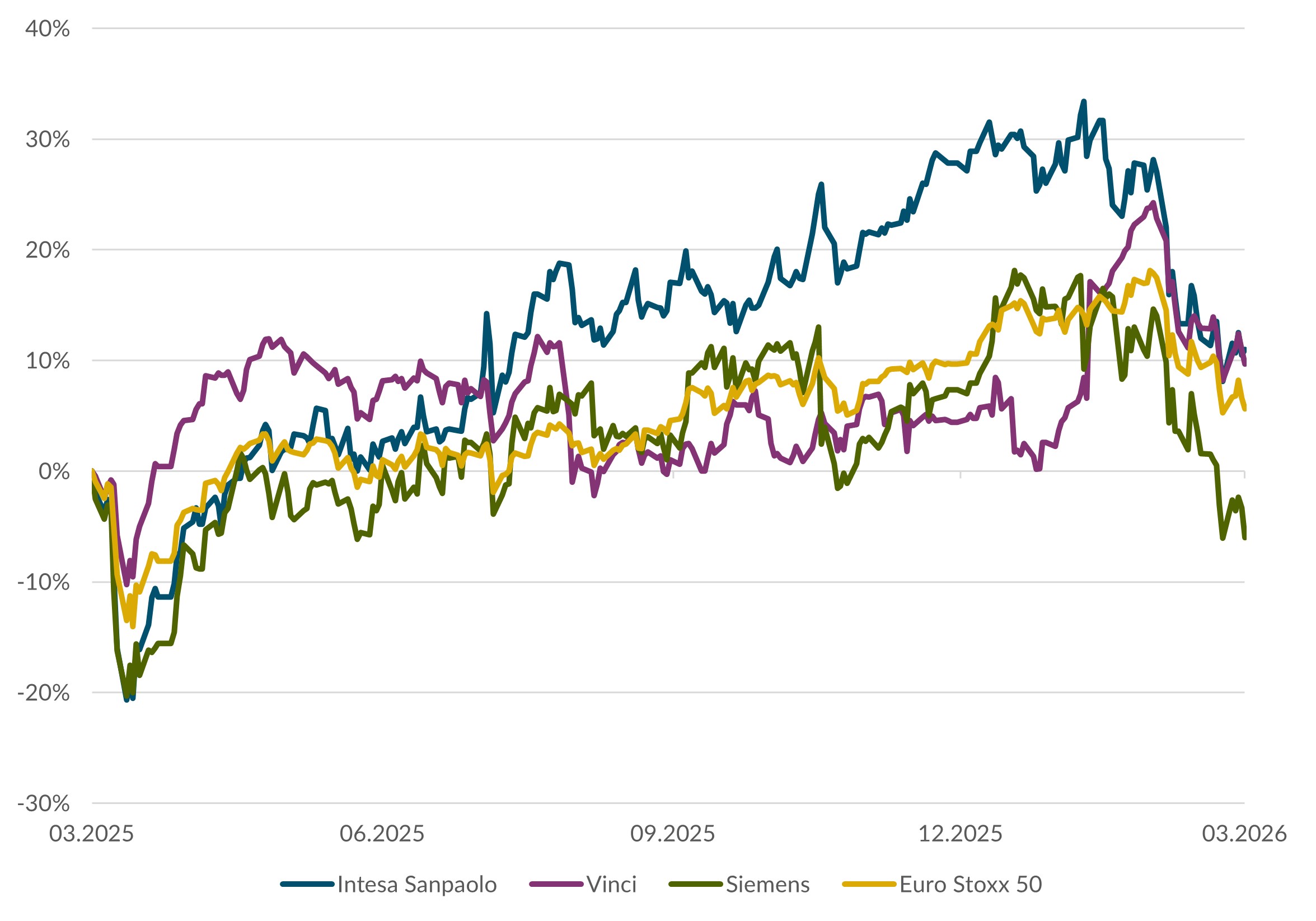

The European Central Bank left key rates unchanged in view of the geopolitical uncertainty. The Iran war has driven up energy costs and is fuelling inflationary fears. Nonetheless, the ECB has stressed that it will not allow a new wave of inflation to materialise. So it would appear that interest rates are set to rise in the next few months. We are remaining cautious over the short term. Over the medium term, however, we are positive owing to fiscal measures and planned capital investments. (wan)

US equities

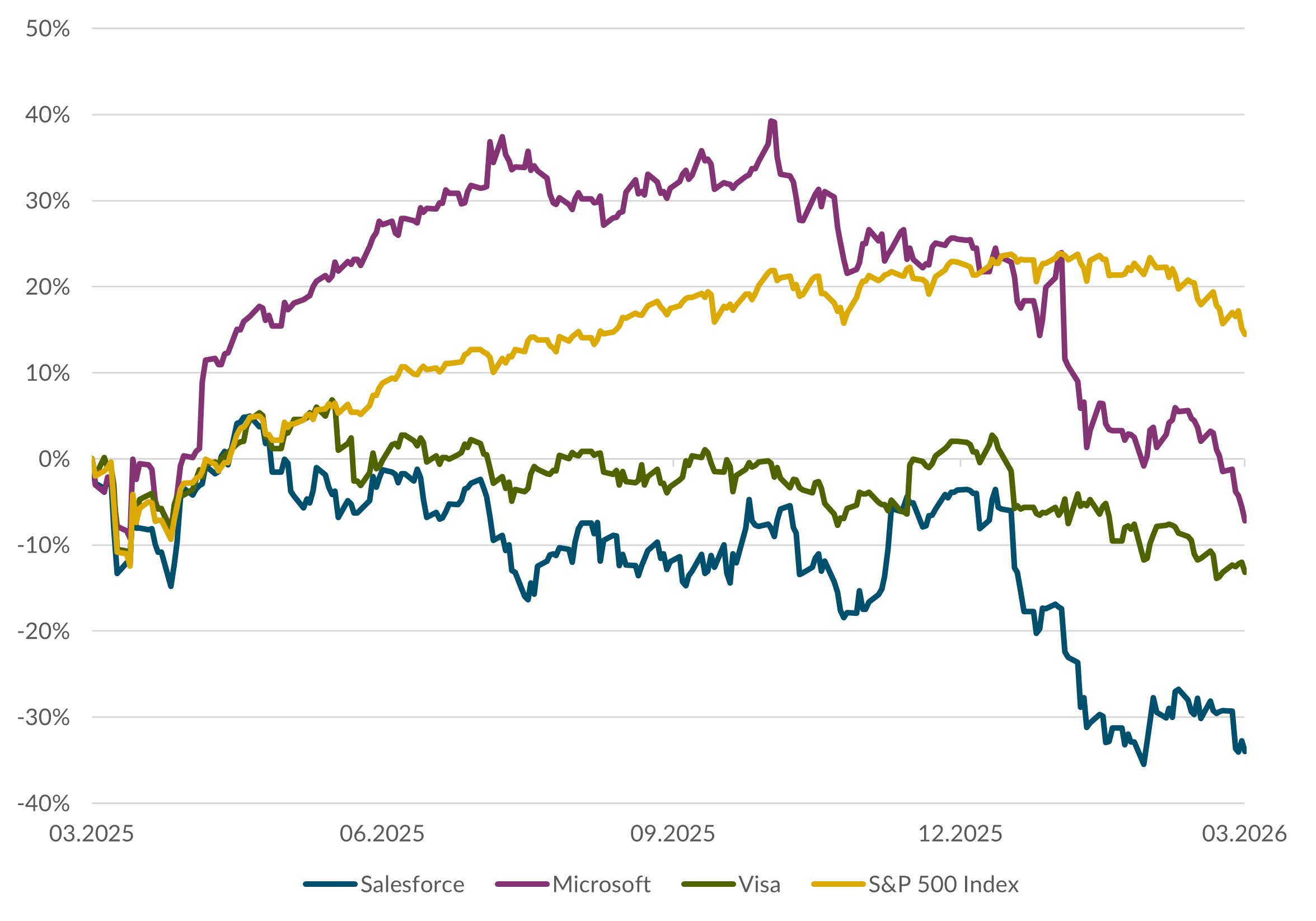

The first quarter was chaotic for the US equity markets. Geopolitical decisions drove performances down from an initial positive position into negative territory. Uncertainty and fear are dominating the market. Share prices may stay volatile for as long as the Iran situation and its effect on oil prices remain unresolved. We remain positive for the US market over the longer term. The lower prices offer good purchasing opportunities for quality stocks over the long term. (amm)

Bonds

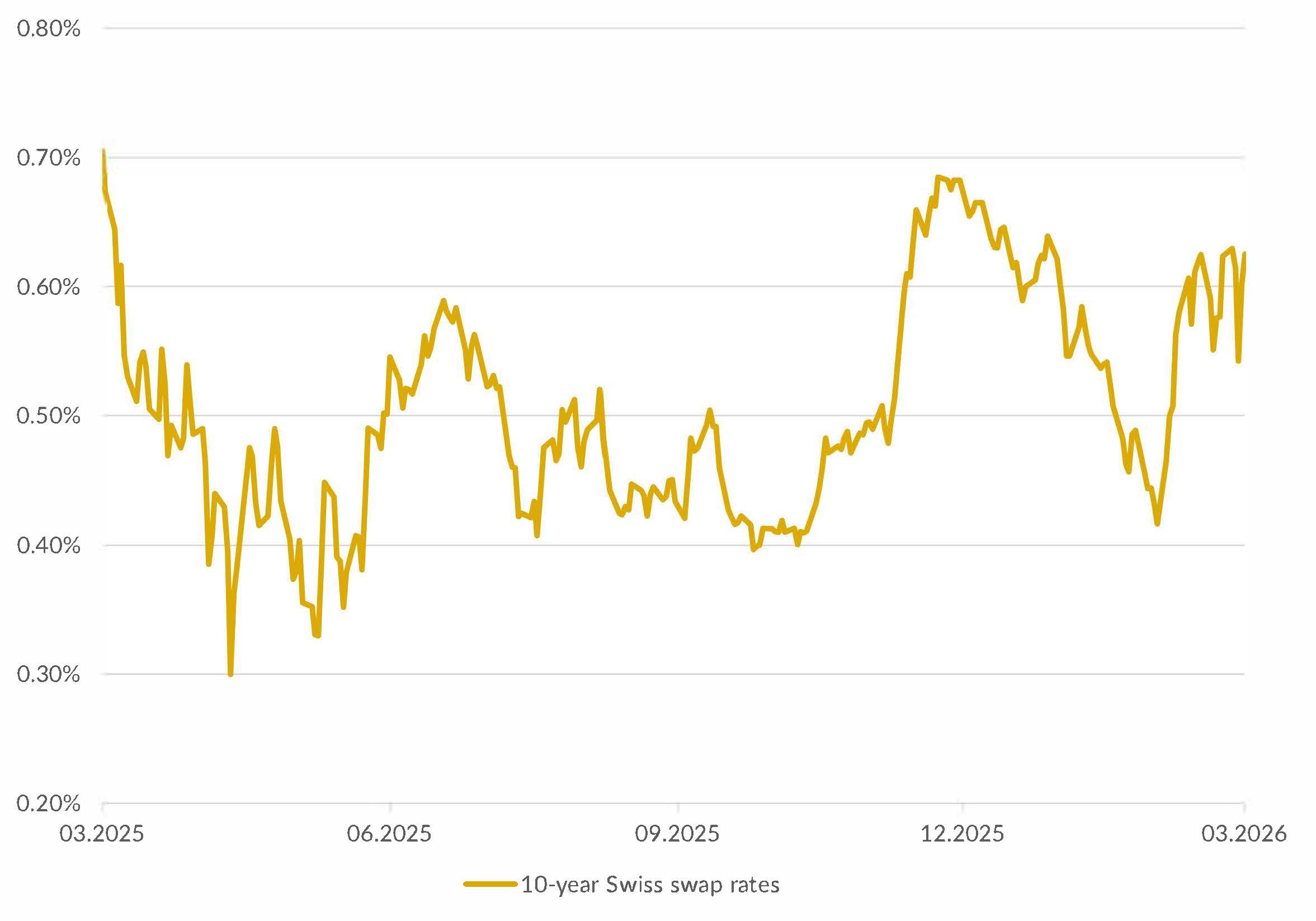

Bond market volatility has recently increased as a result of trading and geopolitical developments. Uncertainty regarding a second wave of inflation led to a rise in interest rates at the short end of the Swiss yield curve, while economic uncertainty resulted in a slight fall at the longer end. Credit risk spreads, on the other hand, remained stable. In the current environment, we are remaining underweight on this asset class and maintaining a slightly lower interest rate risk relative to the market. A continuation of the rise in yields that started in late February may offer a future opportunity to add bonds with higher yields to the portfolio – provided there is no global downturn. We are continuing to focus on corporate bonds from solid borrowers in medium maturities. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Carl Münzer (muc), Andreas Weiss (wan)

Important information

This document constitutes advertising according to the Swiss Financial Services Act (FinSA). It is intended for information and marketing purposes only. The information it contains does not constitute an individual recommendation, an offer, a solicitation to issue an order to purchase or sell securities or other investments, or legal, tax or any other form of advice. Any statements and forecasts included in this document are for information purposes only and are subject to change at any time without prior notice. Bank CIC (Switzerland) Ltd. makes no warranty as to the completeness, reliability, accuracy and timeliness of the information contained in this document. Forward-looking statements and forecasts are based on current assumptions and assessments and therefore do not constitute reliable indicators of future events. The bank accepts no liability for any damage arising from the use of the information and statements provided in this document. This document is not the result of financial analysis and is consequently not required to comply with the statutory regulations concerning the independence of financial analyses. The sending, import or distribution of this document and copies thereof to the United States or to US citizens (within the meaning of Regulation S of the US Securities Act of 1933) is prohibited. This also applies to other jurisdictions that consider such actions to be in breach of their applicable laws.