Perspectives 03/2025

- 7 July 2025

- Insights

- Author: Luca Carrozzo

- Markets

Did you go to Art Basel this year? During the fair, which is held every year and regarded as the biggest contemporary art event in the world, the city of Basel turns into a centre for creativity and dialogue – and sometimes even speculation. A look at the numbers shows that world-famous galleries once again sold big names for high prices this year.

But what do the world of art and financial markets have in common? More than you might suspect at first glance, I would say. Just like on the stock market, it is not always immediately apparent why a work or a security is suddenly the centre of attention – but in both worlds, quality, substance and vision rise to the top over the long term.

That brings me on to a story you may have heard about the Spanish artist Pablo Picasso in a café near Notre-Dame in Paris. A lady once spotted him and asked him to do her a small sketch on her napkin. Picasso obliged, drew something in a few seconds and then said politely: «That will be 10,000 dollars.» The lady was outraged. «But it only took you 30 seconds!» He smiled and replied: «No madame, it took me 40 years.»

As well as being amusing, this anecdote highlights key aspects that matter in the world of art as much as in the financial markets: experience, timing, a trained eye and the knowledge that true value is rarely created overnight. Given the current geopolitical tensions, the rising attention investors are paying to central bank policy and the forthcoming quarterly company reporting season, the significance of these qualities is becoming increasingly apparent.

As a Swiss bank with regional roots and an international outlook, we support our clients with experience, sensitivity and a clear eye for what matters. This issue of CIC Perspectives combines analysis with intuition – well founded, varied and with a pinch of inspiration from the art world.

Luca Carrozzo

CIO

Economic prospects

US politics are unpredictable and volatile and geopolitical challenges are continuing to flare up, making permanent change the only constant at the moment. In particular, US trade policy has had the effect of pulling the timing of the production and export of goods to the USA forward. Economic data have been distorted as a result. For example, Swiss external trade and economic growth were extremely positive in the first quarter. Over the same period the USA (Switzerland's biggest trading partner) reported a record trade deficit (imports were more than exports) and an economic slowdown. These distortions will even out again over the coming quarters, but until that happens it remains challenging to rank and interpret the data.

Back to a low interest rate environment

In March 2024 the Swiss National Bank was the first central bank in the G20 to declare victory over inflation. Just over 15 months and six rate cuts later, the benchmark Swiss interest rate is now at zero once again. The SNB will be sure to think hard before bringing back negative interest rates because of the adverse side effects (on savers, pension funds and the stability of the financial markets, for example), but Switzerland is only one step away from this.

The latest SNB forecasts indicate inflation is likely to rise again slightly in the medium term and growth will remain low at 1-1.5%. The biggest risk to the SNB doing its job of ensuring price stability and taking account of economic performance currently comes from events abroad. (muc)

Markets

Not just risks – opportunities too

News about geopolitics and the economy has been almost entirely negative, but there is light at the end of the tunnel. We have to assume that sooner or later the geopolitical situation will calm down a little and the Fed will loosen its extremely tight monetary policy. Interest rates are low and heading lower. Companies are in a good position and equity market valuations are fair. Investors should not allow themselves to be distracted by high short-term volatility and stick to their long-term strategy. (bae)

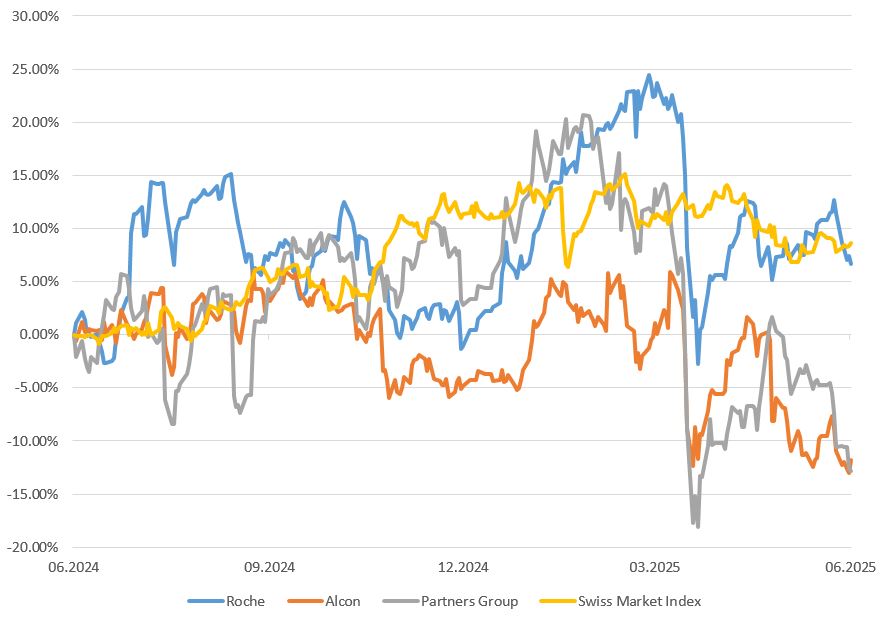

Swiss equities

The SNB cut its benchmark interest rate to zero again in June, so people in Switzerland are once again under pressure to invest. The 3% dividend yield and the high weighting in defensives will support the Swiss equity market. Any setbacks should therefore be consistently exploited to add to top-quality stocks. Among large caps, we prefer Roche, Alcon and Partners Group; in second liners, we like Tecan, Comet and SIG Group. (bae)

European equities

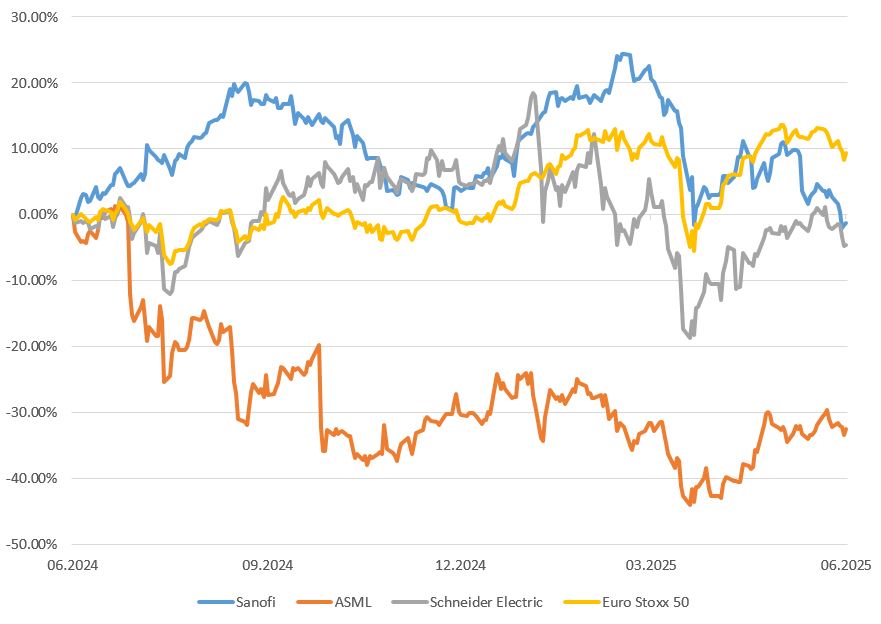

The ECB cut its benchmark rate once again on 5 June – the eighth reduction since mid-2024. GDP growth is now expected to be lower (1.1% instead of 1.2%) and inflation higher (2% instead of 2.3%). Uncertainty over trade policy is holding back investments and exports. However, rising public spending on defence and infrastructure will support growth over the medium term. Our focus is on cyclicals and high-quality stocks. Our recommendations for Europe are still ASML, Sanofi and Schneider Electric. (wan)

US equities

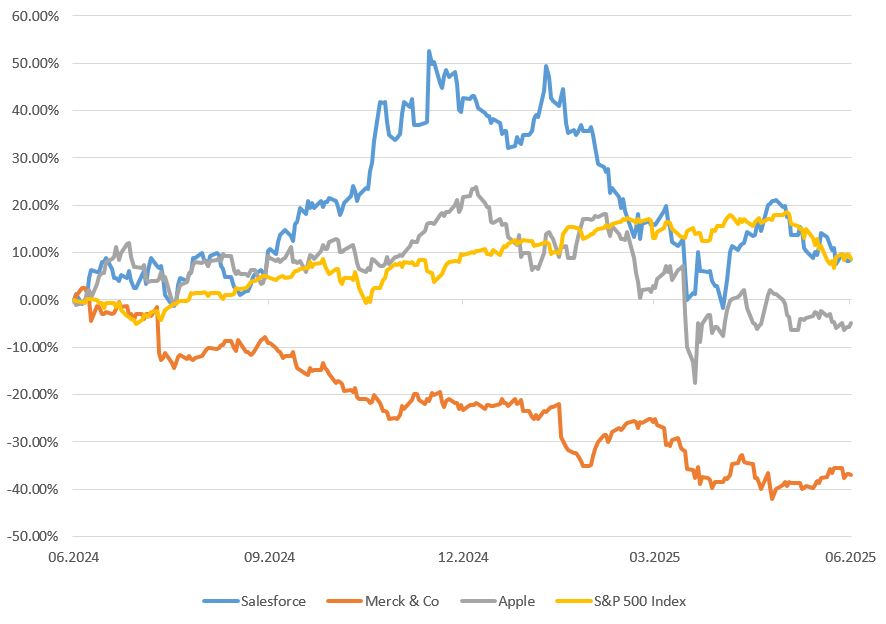

Liberation Day briefly put markets under heavy pressure. In the months since then, however, the US markets have recovered and now stand higher than they were at the start of the year. Uncertainty continues to dominate. The Trump presidency, the war in Ukraine and the tensions in the Middle East are just some of the issues markets are currently having to deal with. We see the US markets moving sideways with volatility over the summer. We recommend Salesforce, Merck and Apple. (amm)

Bonds

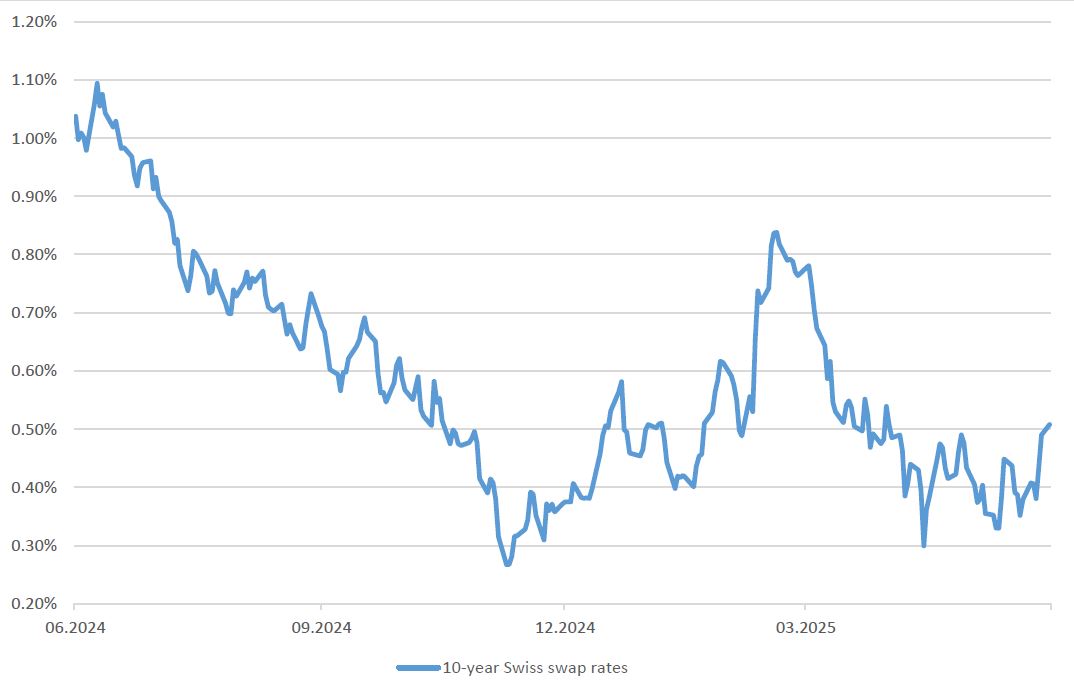

The Swiss bond market has been recovering recently from its correction in March. This has been helped by the fact that Swiss consumer prices fell further in the second quarter. Even though safe havens are in demand in the current environment, Swiss bonds are becoming increasingly unattractive in terms of yield due to the low interest rate environment, with the benchmark Swiss interest rate at 0%. The potential for capital gains is likely to be limited accordingly. We are focusing on corporate bonds from sound borrowers (rated A or better) in short to medium-term maturities. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Carl Münzer (muc), Andreas Weiss (wan)