Perspectives 04/2025

- 6 October 2025

- Insights

- Author: Luca Carrozzo

- Markets

US presidents have traditionally respected the independence of the Fed – in the same way you trust a doctor even when the medicine tastes horrible. Previous holders of the office have grasped that the Fed sometimes has to take decisions that are unpopular, even when they are politically awkward in the short term, just as eating healthy food is sensible, even though it doesn’t always look that inviting.

But things are different with Donald Trump. Ever since he took office in January 2025 his style of communicating with the Fed has been direct. Right from the start he has been a persistent critic of the central bank. He has described its Chair Jerome Powell as an “idiot”, a “numbskull” and a “total disaster”, accusing the Fed of harming the US economy by being too slow to cut interest rates.

Everyone knows the president has an interest in rates being lower and in this context has been putting the members of the Federal Reserve under pressure. He is applying his usual strategy; first he steps up the pressure on individual members of the Fed by speaking in public. Then his administration looks for ways to cast doubts on their integrity. In the case of Jerome Powell, he has accused him of allegedly spending billions on renovating the Fed headquarters in Washington DC, calling it a fraud.

So far the Fed has refrained from responding to Trump's demands. But every time a member of the Fed steps down he has an opportunity to extend his political influence on the committee of the central bank. Trump has left no doubts about what he intends to do. He recently told journalists at a cabinet meeting: “We’ll have a majority. So that’ll be great”. The way for Trump to boost his influence over the Fed may become clear in May 2026 when Jerome Powell’s term as Chair expires. His term as a member of the Fed doesn’t actually end until January 2028, but normally the departing Chair leaves the bank entirely when they step down. This could give Trump the chance to drive his agenda forward inside the Fed.

So far the financial markets haven’t been too worried about all this. As long as the bond market doesn’t react negatively to attacks on the independence of the Fed, the Trump administration sees no reason to alter its stance. But that could change quickly. Trump’s attacks on the integrity of the central bank could have long-term consequences. It’s not unreasonable to draw a comparison with authoritarian leaders in emerging markets. For example, President Erdoğan of Türkiye tried to exert influence over monetary policy the way he wanted, ultimately wrecking confidence in the country’s economic policy, pushing the currency down and driving consumer prices sky high.

Don’t forget that, on current estimates, the USA pays roughly USD 2.5 billion a day in interest on the country’s national debt. This vast sum is the result of the huge level of government borrowing, in excess of USD 36 trillion, and now accounts for a major item in the federal budget. If investors lose confidence in the independence of the Fed, US funding costs could rise considerably and put even further strain on the budget.

It’s fair to say it takes time to trash the credibility of an institution like the Federal Reserve, but the consequences of a loss of trust have the potential to unleash shock waves. The stability of the largest economic power in the world is at stake – and with it, confidence in the entire financial system. So it is absolutely essential to preserve the integrity and independence of the Federal Reserve if long-term economic security is to be maintained.

Luca Carrozzo

CIO

Economic prospects

As anticipated, after a strong start to the year (+0.7% in Q1), the second quarter saw only marginal growth of +0.1%, a consequence of pull-forward effects (exports and investments were brought forward due to uncertainties and the threat of changes). Lack of clarity over trade policy and a range of geopolitical risks are having a negative impact on investment sentiment and clouding prospects. Growth in the economy in the second half is therefore expected to be only modest. The forecast for the full year is just over 1%.

Innovation and digitalisation are key

For an exporting country like Switzerland, the current environment is undoubtedly a challenge. The objective is therefore to cushion existing handicaps as far as can be done, and if possible even make up for them. This is also a matter for politicians. Taking action to reduce administrative burdens and promoting structural change, innovation and research in a targeted manner can strengthen the Swiss economy and support sustainable growth.

Digital technologies and artificial intelligence have the potential provide a permanent boost to productivity and added value. But this requires companies to invest in their organisations and the qualifications of their staff. Large companies and modern service providers in particular are using digitalisation to refocus their business models and processes – but many SMEs are being more cautious. The task facing Switzerland is to actively seize the opportunities offered by digitalisation, maintain its policy of innovation and remove obstacles swiftly to ensure Swiss companies remain competitive. (muc)

Markets

High likelihood of a year-end rally

Despite the ideas of the Trump administration changing almost daily, equity markets gained even over the traditionally problematic summer months. In Switzerland and Europe, advances were relatively modest, but in the USA stocks rose strongly as the tech sector posted double-digit profit increases. After a feeble start to the year, Wall Street is now back among the leaders. An economic recovery in Europe, declining interest rates in the USA and rising company earnings are laying solid foundations for a year-end rally. (bae)

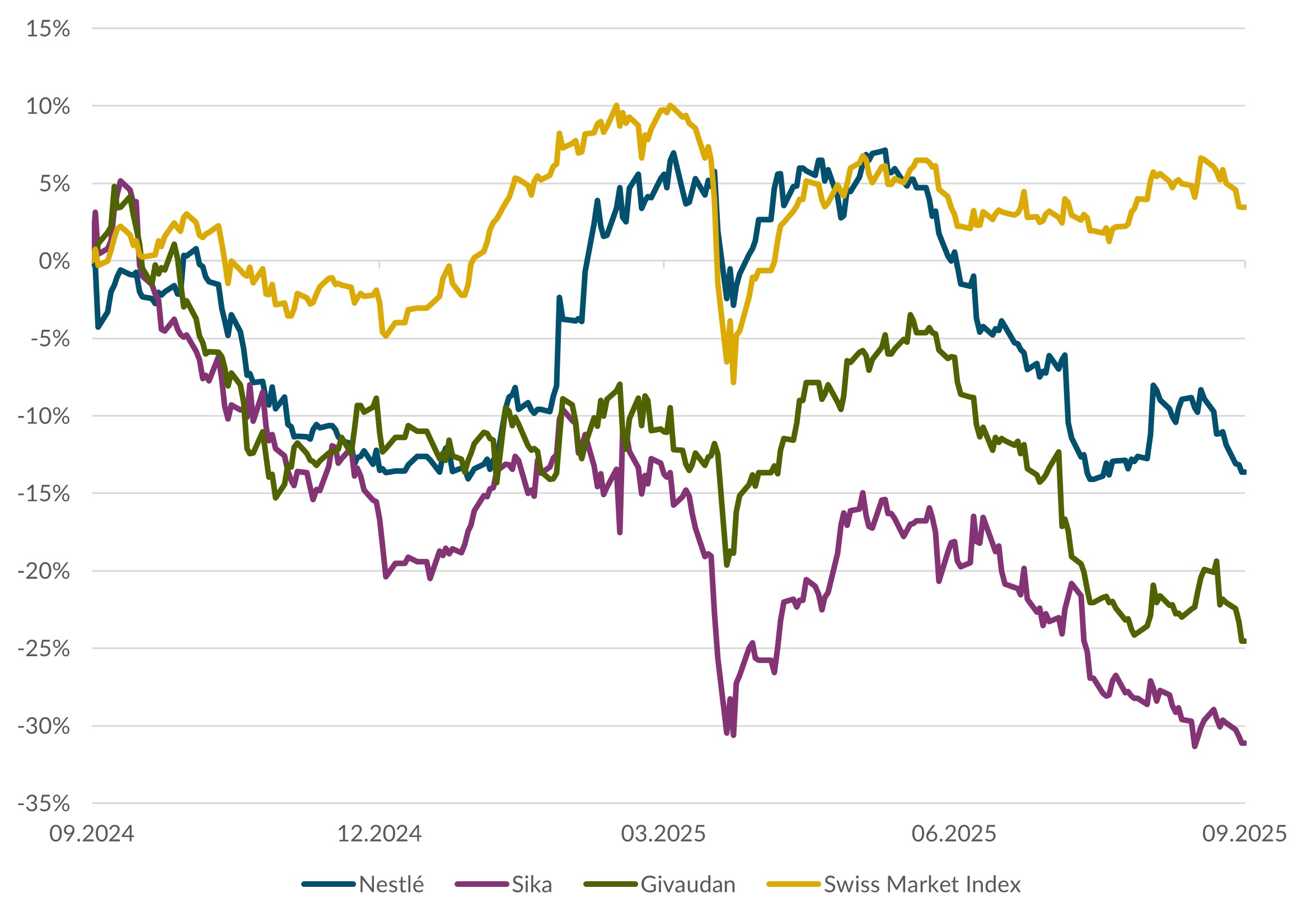

Swiss equities

The Swiss equity market has again been a disappointment by international standards. This has been driven not so much by the 39% tariff on Swiss goods exports to the USA as the poor performance of the two index heavyweights Roche and Nestlé. Now that Nestlé has replaced the two people at the top of the company, we anticipate a rapid series of confidence-building measures that will generate a sharp recovery in the stock price. Among large caps, we prefer Nestlé, Sika and Givaudan; in second-liners, we like Bachem, Georg Fischer and VAT Group. (bae)

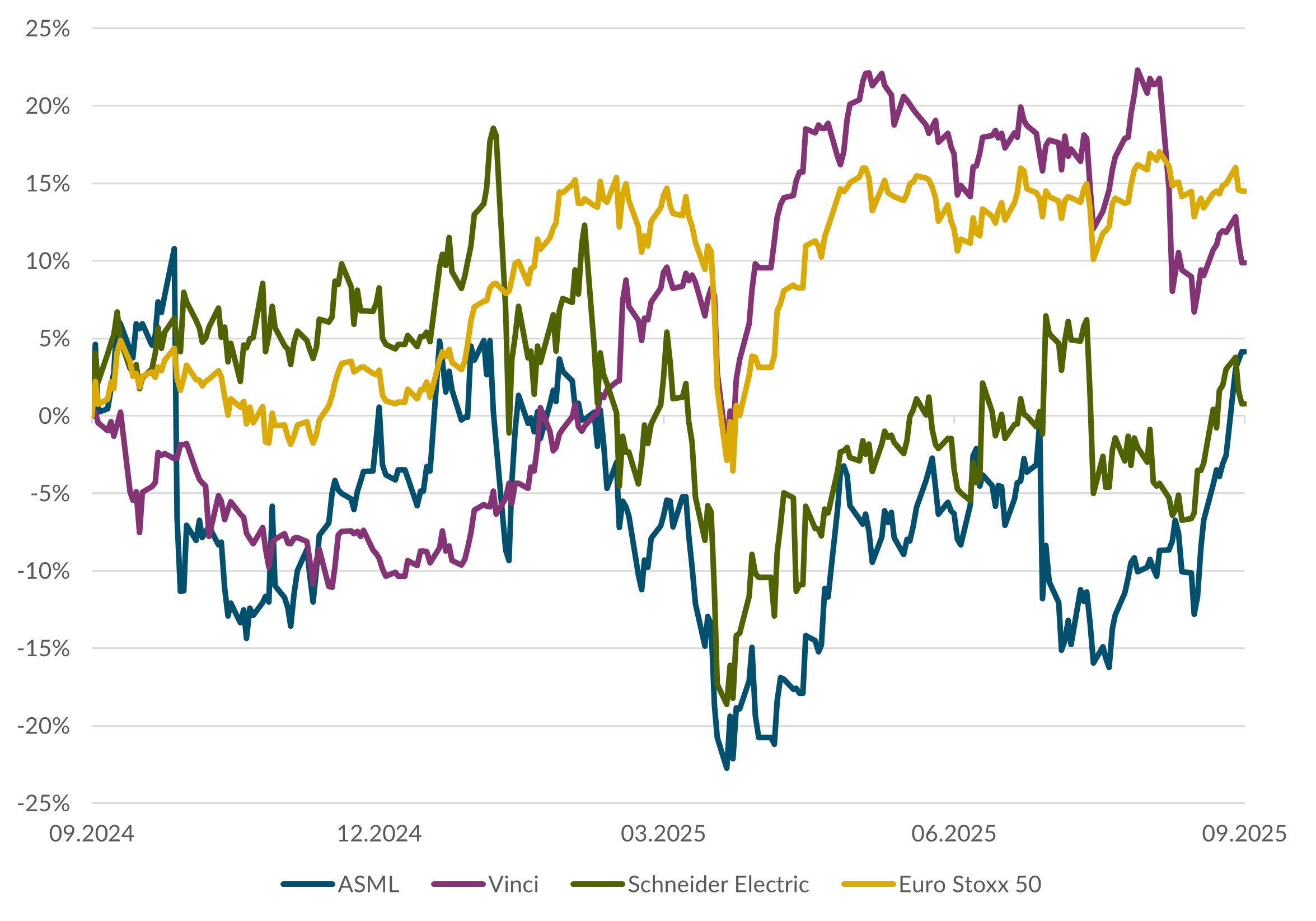

European equities

Economic growth was stronger than expected in the third quarter of 2025. This led to the ECB deciding to hold off from any further rate cuts for the time being. In the short term, another government crisis in France and the subsequent rating downgrades are holding European stocks back. In spite of these obstacles, the leading indicators are pointing to a moderate upturn. We remain positive on European equity markets. Our recommendations for Europe are ASML, Vinci and Schneider Electric. (wan)

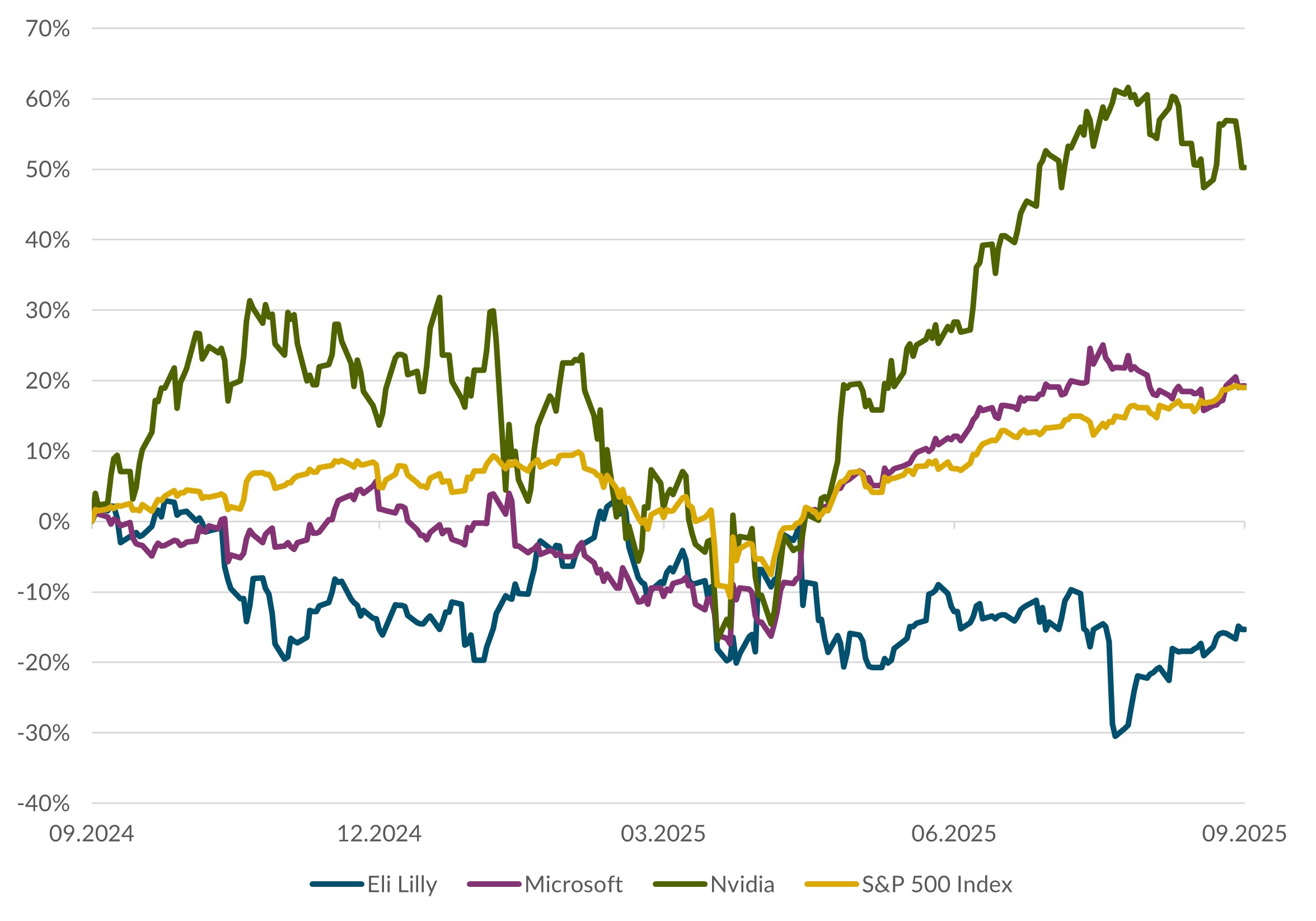

US equities

In his speech at the Federal Reserve's Jackson Hole Economic Symposium, Fed Chair Jerome Powell drew attention to the risks to the labour market, but also highlighted the risk of inflation being more persistent. By doing so, he paved the way for a rate cut without committing to do so at the next meeting. The sustained attacks on the Fed by Donald Trump, on the other hand, gave cause for concern. Overall, falling interest rates, rising company earnings, capital expenditure, private consumption and the momentum in the AI industry are likely to have a positive effect on markets. We recommend Eli Lilly, Microsoft and Nvidia. (amm)

Bonds

The Swiss bond market posted a positive performance in the third quarter, with rates beyond five years falling. Credit spreads remained stable. In the current environment, Swiss bonds offer reliable but increasingly modest yields. The average yield on investment-grade Swiss bonds is now 0.67%, putting investors in something of a quandary. A degree of flexibility is therefore required when selecting and allocating assets. We continue to focus on corporate issues from solid debtors in medium maturities. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Carl Münzer (muc), Andreas Weiss (wan)