Perspectives 01/2026

Another year is behind us. We can look back on 2025 as a period of positive equity markets, sustained low interest rates, political uncertainty and plenty of action from central banks. Now we have all digested our Christmas turkey and mince pies, it's time to look ahead – to all the opportunities and challenges 2026 will bring.

- 12 January 2026

- Insights

- Author: Luca Carrozzo

- Markets

In this issue of CIC Perspectives, we take a peek into the future of the world of finance and show you the latest and most promising investment trends with the potential to have a lasting impact on your strategy. Change and dynamism are constant companions in the economy and on the stock exchange.

New Year's greetings combine personal hopes with business success and remind us of our responsibility to you, our clients: to accompany you on the path to long-term wealth preservation and sustainable growth. We apply transparent and responsible investment decisions to create stable value and strengthen your trust on a lasting basis.

We hope the coming year will be one of smart decisions and resilience, and that economic strength and the common good will remain in a healthy balance. On that note, I would like to wish you a healthy and successful New Year and thank you for the trust you have placed in us.

Luca Carrozzo

CIO

Economic prospects

Last year was marked by a range of different uncertainties. Like other countries, Switzerland was hit by US tariffs, below-average growth rates and geopolitical risk. In the domestic labour market, this was particularly apparent in export-oriented industries and cyclicals. The rise in the unemployment rate was modest, however.

The Swiss franc was strong, and one of the main reasons inflation stayed low last year. For long periods, though, this hovered at or around the level of price stability the Swiss National Bank aims for. Despite volatile external trade having a considerable effect on performance, the Swiss economy once again demonstrated its resilience. In this context, we anticipate growth of around 1.4% for 2025 as a whole.

Time for fresh perspectives

The State Secretariat for Economic Affairs is predicting growth of 1.1% in both Switzerland and the euro area in 2026. In the USA, it is expected to be 1.7%. So 2026 will probably be another year when we are reminded that growth has its limits.

Although plenty of risks lie ahead, things look a little more balanced when considering the opportunities. Challenges on the trade front have eased for the time being and inflation expectations are under control in many places. Benchmark interest rates may be cut further and investments in the tech industry look set to be maintained. In addition, continued fiscal policy activity in the USA, Europe and China could help to give global trade some impetus once again.

Overall, opportunities are emerging that could lay the basis for the economy and financial markets to put in a good performance in 2026. (muc)

Markets

Positive start to the year expected

Equity markets rose by double-digit amounts last year. Even so, we expect them to go up again in 2026. Weak growth with moderate inflation, low interest rates in Europe and the prospect of further cuts in the USA, double-digit corporate earnings growth, rising infrastructure expenditure and pressure to invest due to unattractive bond yields, as well as the higher likelihood of a peace agreement in Ukraine, are all factors suggesting equity markets will get the year off to a pleasing start. (bae)

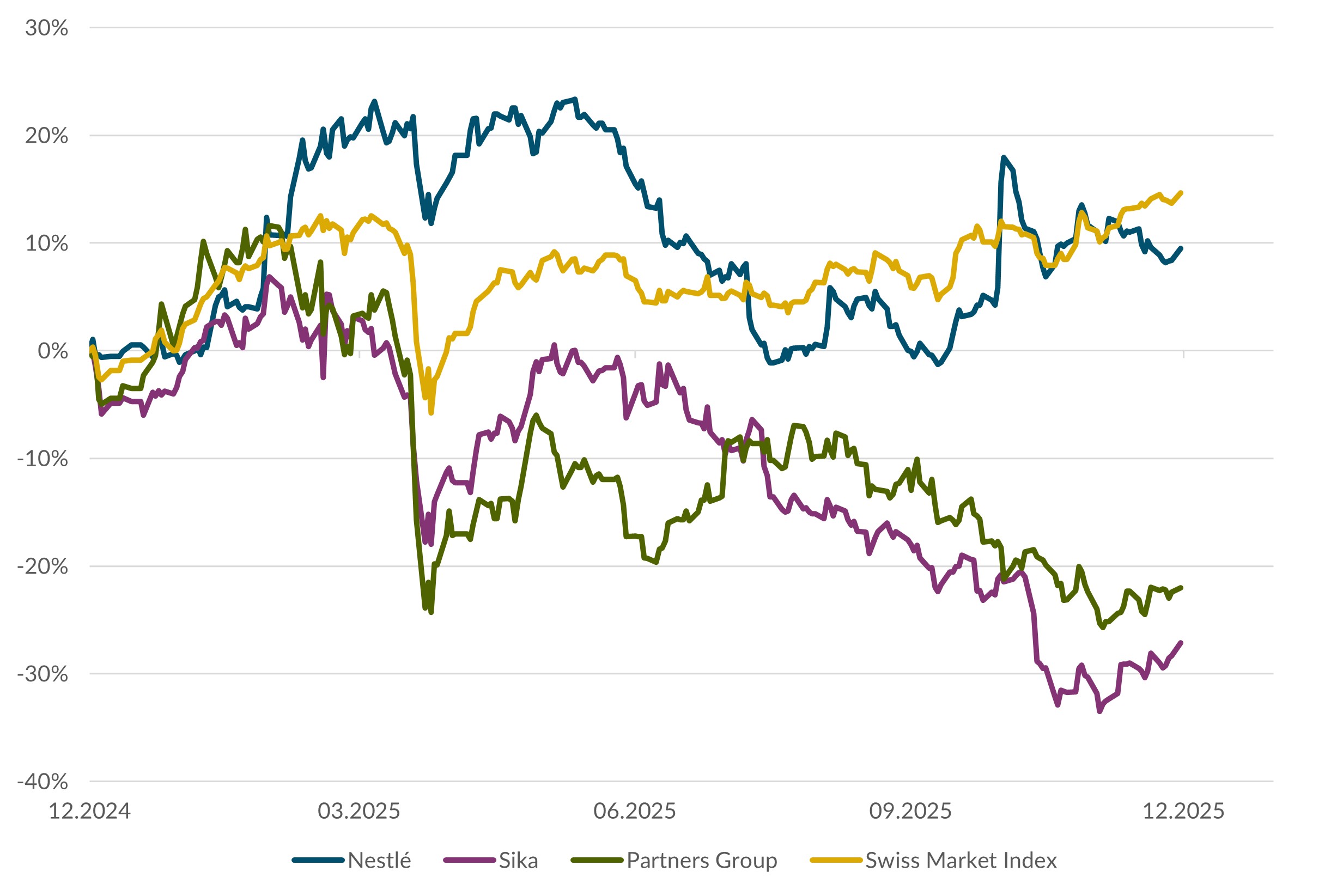

Swiss equities

The Swiss equity market was among the winners in the fourth quarter thanks to a double-digit advance by index heavyweight Roche. The monetary policy of the SNB remains expansionary and the tariff deal with the USA has lifted the mood among Swiss companies. 2025 saw some large differences in the performance of individual stocks, sometimes even within the same sector. We expect a correction at the start of the year. (bae)

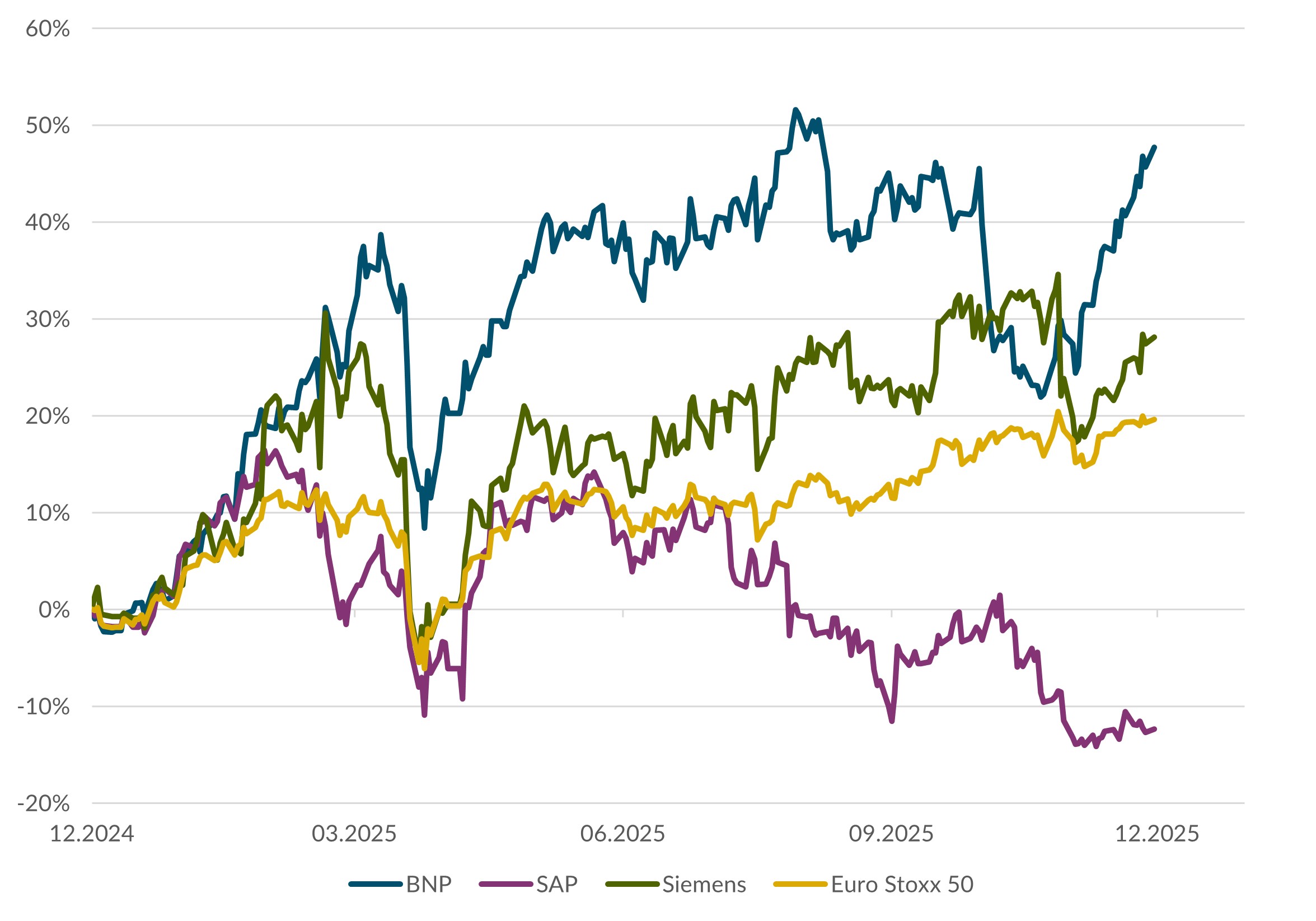

European equities

The ECB has probably reached the end of its cycle of monetary loosening. Lower energy prices, stiffer competition and slower wage growth will bring core and overall inflation below the central bank's target in the months ahead. This will allow companies to restore margins. The European economy has lost some momentum, but the domestic factors are strong enough to allow a recovery in 2026. We remain positive on European equity markets. (wan)

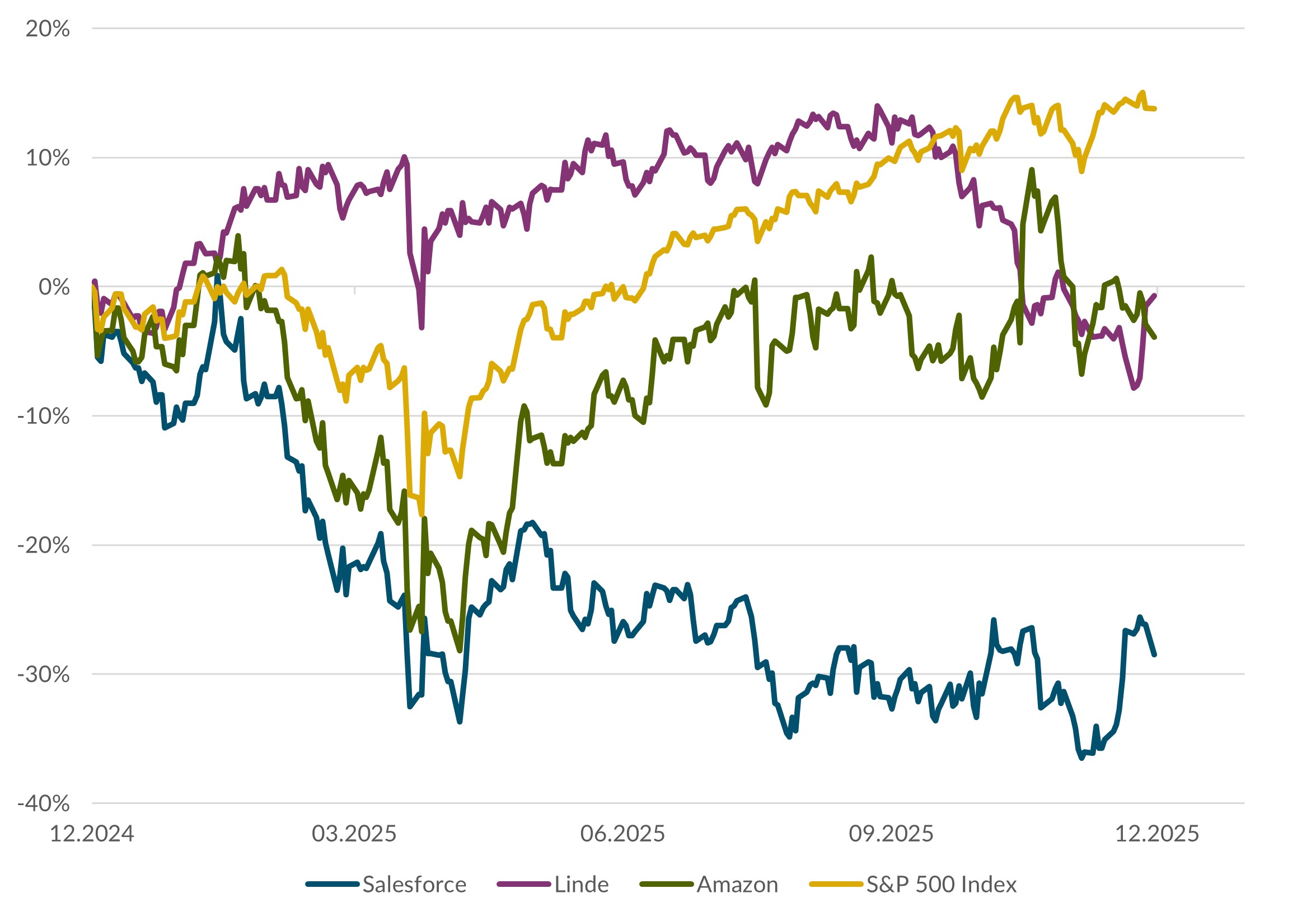

US equities

2025 was another strong year for US equity markets. The good performance was driven by Fed rate cuts and the boom in AI stocks. 2026 could be a positive year for equity markets as well. The anticipated rate cuts in the USA will further excite investor interest. Huge sums that have been parked in money market funds are likely to find their way into equity markets if rates go lower. (amm)

Bonds

December saw an unexpected rise in long-term yields all over the world. The combination of sustained economic growth and fears inflation might break out again gave rise to concerns that the global cycle of rate cuts might be drawing to an end. As far as Switzerland is concerned, in the current environment we continue to view corporate bonds from solid borrowers in medium maturities as the most attractive. Yields are so low right now that government and semi-government issues scarcely offer any return – but are exposed to considerable risk if interest rates change. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Carl Münzer (muc), Andreas Weiss (wan)