Perspectives 03/2026

Content for residents of Switzerland (see footnote).

A lot has been happening on the financial markets over the past few months. Solid corporate figures and optimistic outlooks encountered a geopolitical situation of tensions, unexpected U-turns and short-term relief. An environment that opens up opportunities, but also calls for caution.

- 6 July 2026

- Insights

- Author: Luca Carrozzo

- Markets

The agreement reached in mid-June between the United States and Iran on opening the Strait of Hormuz is a case in point. For weeks one of the key global arteries for energy trading had been under pressure, with the impact on prices being significant. Once it reopened the situation quickly eased, oil prices came down sharply and equity markets hit new highs. This is a classic case of how quickly market sentiment can turn when geopolitical conditions change.

This summer, attention has also turned to the FIFA World Cup in the United States, Mexico and Canada. In some ways, this interplay between geopolitical uncertainty and dynamism is reminiscent of the celebration of football in North America. The outcome may seem obvious on paper, but the flow of play often dictates otherwise. Outsiders gain momentum, favourites come under pressure and sometimes a single moment is all it takes to bring about a fundamental change in the situation. That’s just how things are on the capital markets right now. Expectations matter, but what's crucial is how flexibly you can react to new developments.

At first glance, rising markets might suggest optimism, but at the same time they also call for precise risk management. In an environment where political decisions or commodity prices can be reassessed in a flash, the ability to take a nuanced view is essential. The most recent fluctuations in the energy market provide a perfect example of how closely economic trends and geopolitical events are intertwined, and how quickly they can give rise to both new opportunities and new uncertainties.

So this issue of CIC Perspectives is not meant to be a statistical guide, but a snapshot of a match that is still under way. We aim to help you put new developments into context, identify connections and make sound decisions, all the while remaining fully aware that there are no guarantees – either in the financial markets or on the pitch.

Luca Carrozzo

CIO

Economic prospects

The longer the conflict in the Middle East drags on, the more the impact will be felt. Higher energy prices are starting to push up inflation. Global economic growth forecasts have been cut and central banks face the challenge of managing policy so as to ensure price stability without slowing down growth too much.

The Swiss economy got off to a solid start this year after a weak final quarter of 2025. Gross domestic product in the first quarter rose 0.4%. Value added in chemicals and pharmaceuticals was down, but the performance was boosted by industrials. The services sector expanded slightly and consumption held steady.

However, the economic prospects for the full year remain modest – higher energy prices and the uncertain geopolitical environment are having a moderating impact on households’ willingness to consume, and on investment.

The strength of the Swiss franc, combined with weak demand from abroad, is also hurting exporters. We expect Swiss gross domestic product of 0.8-1.0% for the full year 2026, i.e. below the long-term average of 1.8%.

Sport and the Swiss economy

If you take the revenues of Swiss-based sports associations like FIFA, UEFA and the IOC into account, this has a positive effect on economic performance. Estimates suggest this year’s FIFA World Cup football tournament will boost Swiss economic growth by 0.3-0.4%.

This is because from an economic perspective, the revenue such events generate by selling broadcasting and brand rights, sponsorship and other offerings counts as output from an organisation resident in Switzerland. Where the events actually take place is irrelevant. The “FIFA effect” is becoming less significant, however, partly because international sporting events have become more frequent in recent years. In any case, the benefit to the real economy and the labour market is limited. So when measuring economic output, it makes sense to strip out this distorting element. (muc)

Markets

Will the ceasefire hold?

Equity markets gained slightly more than average in the first half of 2026, despite the geopolitical turbulence. Regardless of all the euphoria surrounding AI, we are not in a bubble on the stock market as long as corporate profits rise more than share prices. We expect equity markets to consolidate over the summer, as the ceasefire still looks precarious and the impact higher oil prices have had on company earnings in the second quarter is not yet known. (bae)

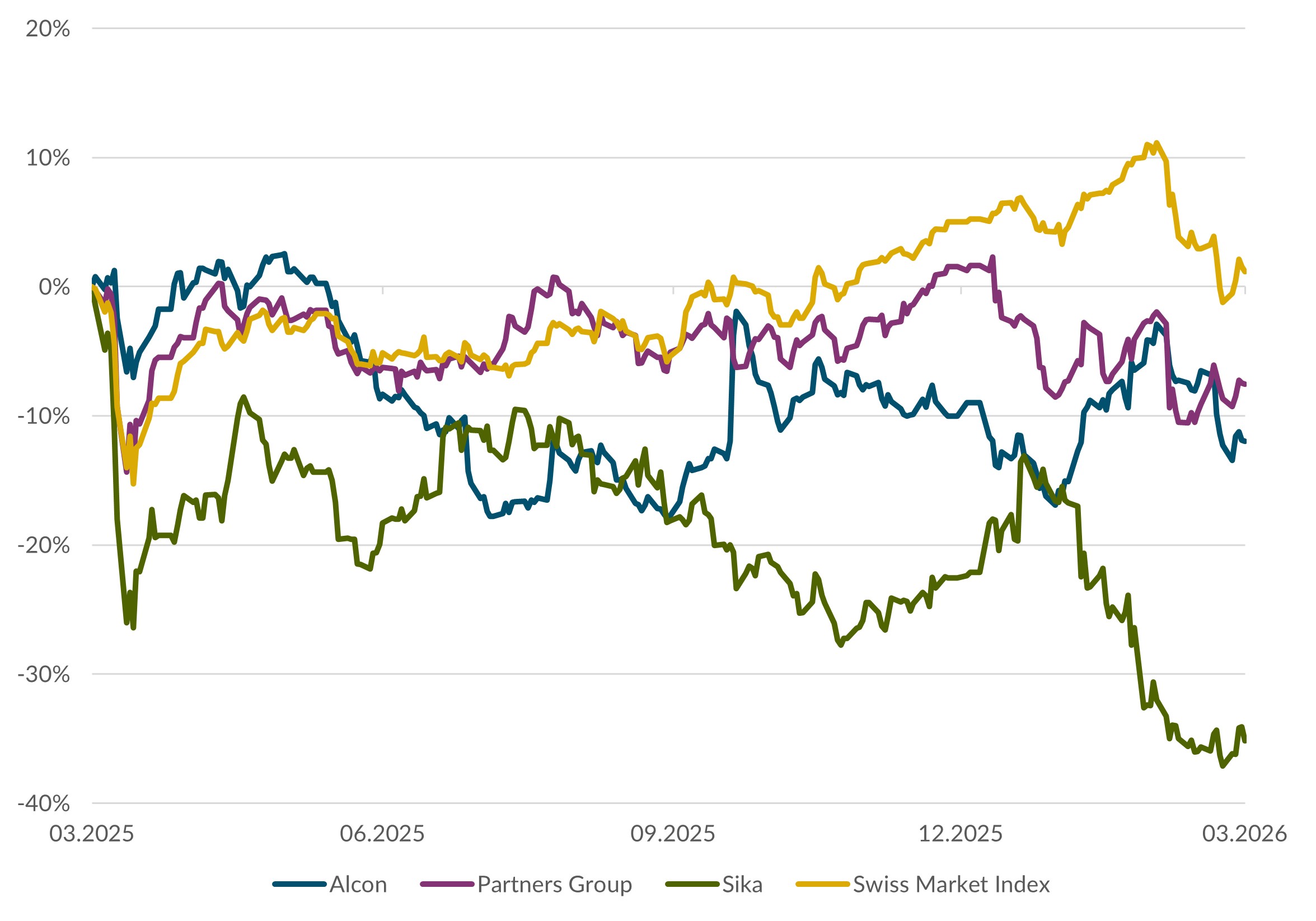

Swiss equities

Unlike other central banks, the Swiss National Bank (SNB) is comfortably placed. The oil price may have shot up, but inflation in Switzerland is still well below 1%, allowing it to leave interest rates at 0%. Hence there is little alternative to Swiss equities, not least because they offer a dividend yield of 3%. (bae)

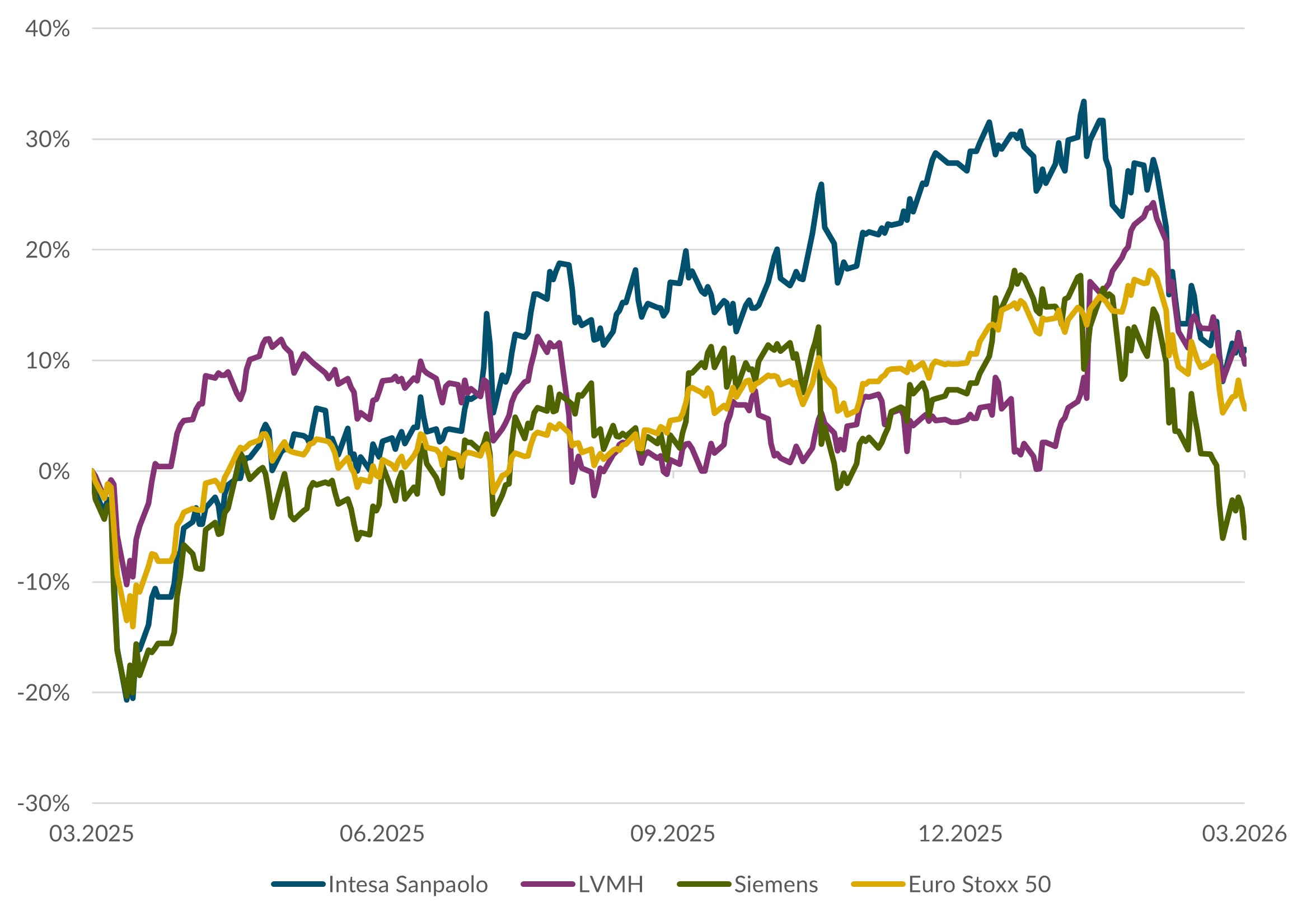

European equities

The European Central Bank (ECB) reacted to rising inflation by hiking its benchmark rate by 25 basis point. The inflation forecast for this year has been raised from 2.6% to 3%, and the growth forecast cut to 0.8%. Private household finances remain in good shape, so consumption is still the most important driver of growth. Investments in new technology and fiscal measures should provide additional support. We therefore remain positive on equity markets. (wan)

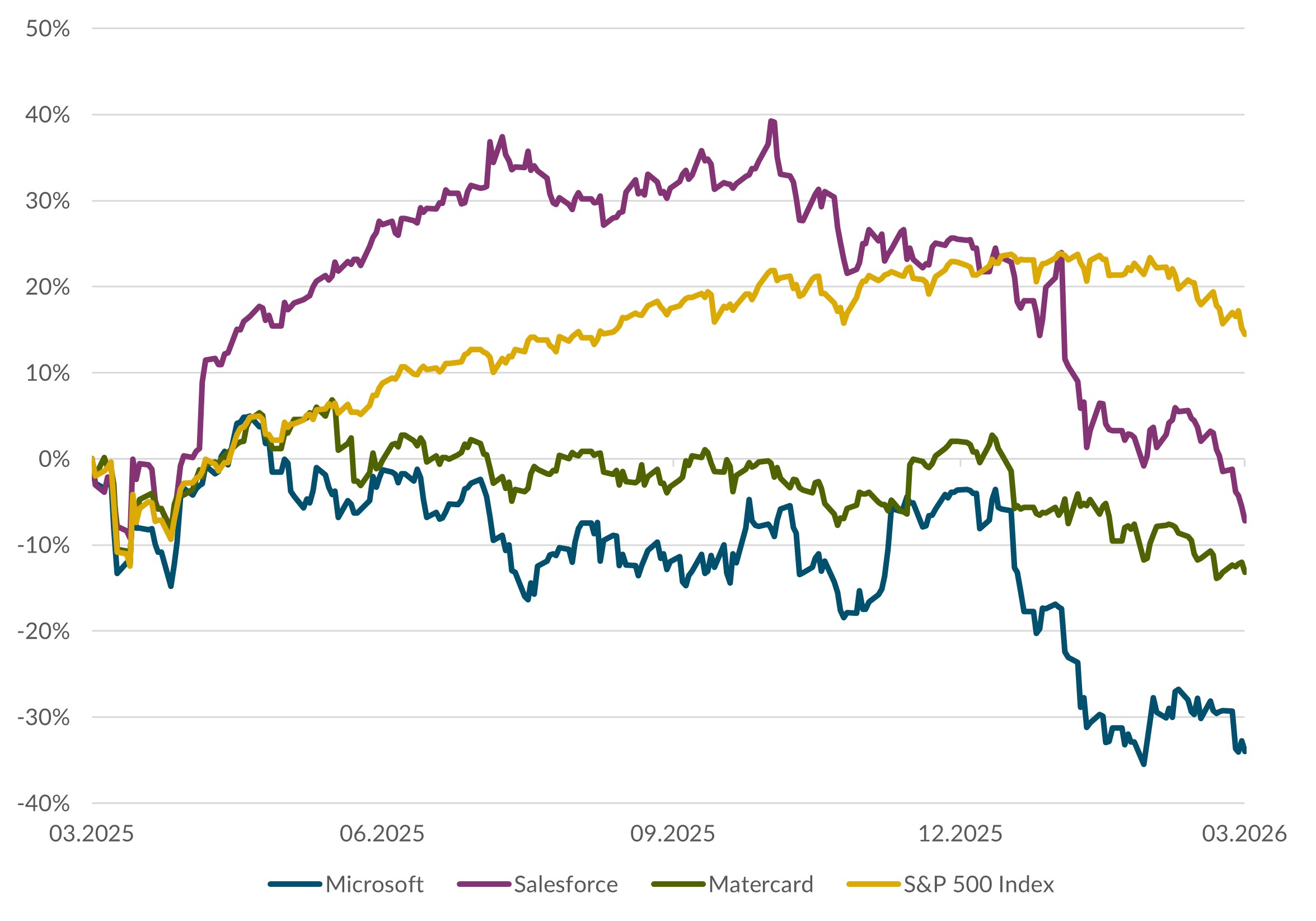

US equities

It was a volatile first half of 2026 for the US equity markets, heavily influenced by geopolitical decisions. Indices hit new highs despite higher oil prices and uncertainty over how long the Iran crisis will last. Once again, it was AI that drove markets upwards. The second quarter results due to be published in July and August will set the tone for the second half of the year. We anticipate that markets will remain volatile, but are positive for the long term. (amm)

Bonds

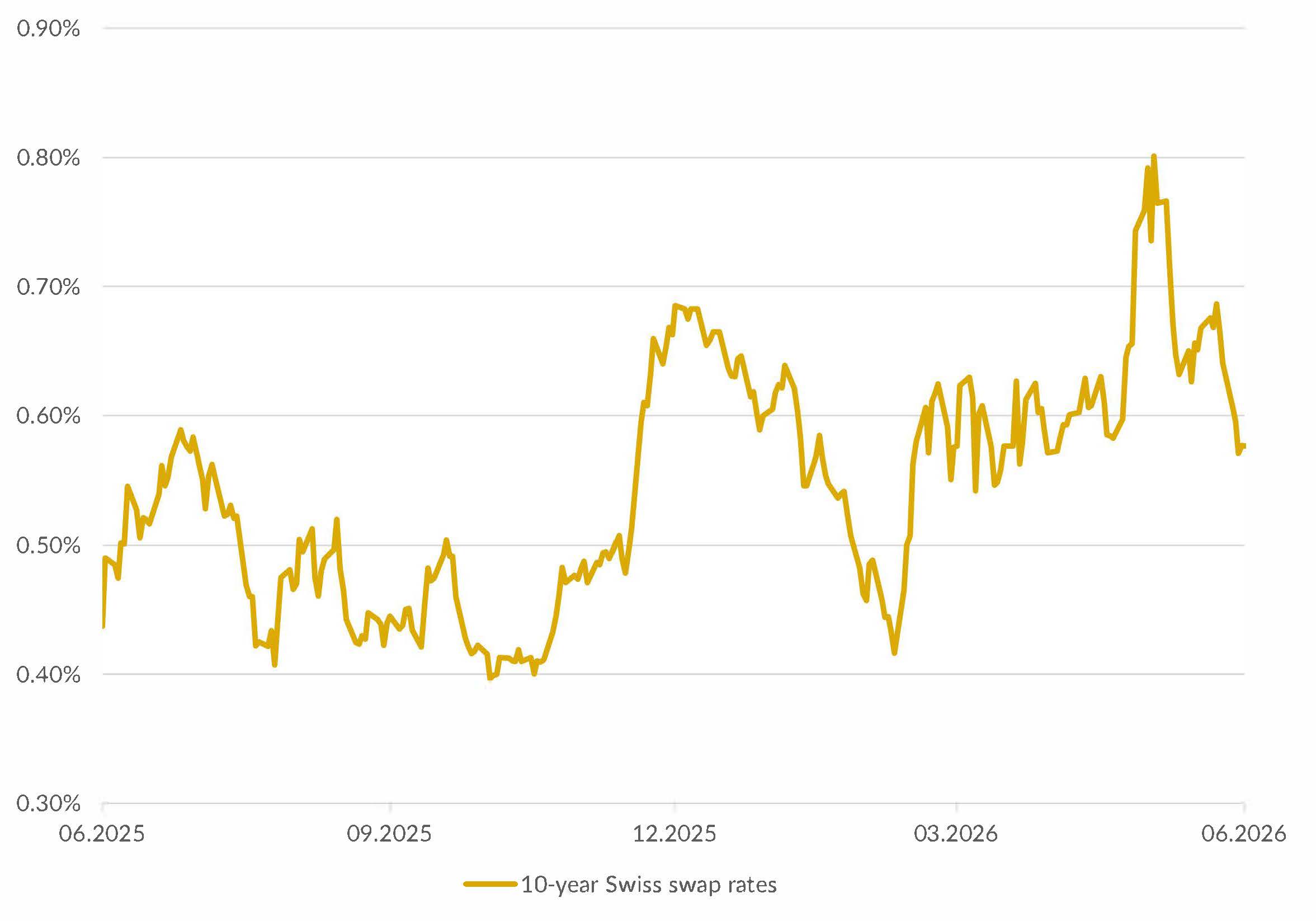

The Swiss bond market has mostly moved sideways in recent months. Since the end of March the short end of the Swiss yield curve has returned to normal somewhat, i.e. flattened, as there is no question of the SNB increasing the benchmark rate in the near future. The credit risk premiums that borrowers have to pay on the capital market based on their creditworthiness have stayed low. In an environment where prices are rising all over the world, economic growth is slowing, geopolitical risks are high and yield levels enticing, shorter-maturity investments are attractive. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Carl Münzer (muc), Andreas Weiss (wan)

Important information

This document constitutes advertising according to the Swiss Financial Services Act (FinSA). It is intended for information and marketing purposes only. The information it contains does not constitute an individual recommendation, an offer, a solicitation to issue an order to purchase or sell securities or other investments, or legal, tax or any other form of advice. Any statements and forecasts included in this document are for information purposes only and are subject to change at any time without prior notice. Bank CIC (Switzerland) Ltd. makes no warranty as to the completeness, reliability, accuracy and timeliness of the information contained in this document. Forward-looking statements and forecasts are based on current assumptions and assessments and therefore do not constitute reliable indicators of future events. The bank accepts no liability for any damage arising from the use of the information and statements provided in this document. This document is not the result of financial analysis and is consequently not required to comply with the statutory regulations concerning the independence of financial analyses. The sending, import or distribution of this document and copies thereof to the United States or to US citizens (within the meaning of Regulation S of the US Securities Act of 1933) is prohibited. This also applies to other jurisdictions that consider such actions to be in breach of their applicable laws.