perspectives 01/2024

Article written on 8 January 2024

2023 was a challenging year for stock markets. Ultimately it drew to a positive end, but along the way it showed us the increasing importance of good risk management. 2024 too has risks investors should not underestimate. There is no end in sight to the wars in Ukraine and the Middle East, and the tensions in the Far East are also unlikely to ease. On top of that, some countries are facing elections which could have consequences beyond national borders or even for the whole world.

At the macroeconomic level, we have to be braced for a hard landing in the USA, a possible recession in the European Union, a slowdown in growth in China and a persistently strong franc acting as a drag on the economy in Switzerland.

But as always in these scenarios, there is also an optimistic side; economies could prove more resilient than anticipated. The forthcoming elections could also have a positive impact and bring stability to the overall economic conditions.

In our view, the fact that the central banks will be providing stronger support to the economy again opens up further opportunities. The packages to expand sustainable energy generation and infrastructure will act as a stimulus, boosting both sustainability and growth.

We are optimistic that 2024 will prove a good year for the markets. The macroeconomic risks may be rising, but there are also opportunities to be seized. This all assumes you have a portfolio that is sensibly invested with nimble and professional management to allow you to react rapidly to major changes in the macroeconomic environment.

Luca Carrozzo

CIO

Economic prospects

The global economy is in a feeble state and concerns about a slowdown are not letting up. Weakening activity is increasingly apparent among exporters and geopolitical tensions are a further drag on sentiment. Nevertheless, the forecasts for Swiss economic growth in 2024 are 1.1%, or 1.5% adjusted for sporting events.

Swiss economy putting in a respectable performance

Next year, just like this year, growth is expected to be positive but similarly below average; compared to other countries in Europe, though, the forecasts are not bad at all.

Overall, the European economy seems to be finding it hard to get back on track after the crises it has been through and is performing below potential. Switzerland, by contrast, has been able to make up for the dip in growth caused by the coronavirus, for example, and is now generating as much value as it was before the crisis. Domestic consumption, and especially the service sector, which accounts for around 75% of Swiss economic output, looks set to put in a solid performance again over the next 12 months. The extraordinarily low level of unemployment and stable prices within the SNB’s target range should continue to have a steadying effect on the tertiary sector. Even in an environment where external trade is subdued because of the global economic weakness, Switzerland has the potential to come through this transitional phase relatively unscathed. (muc)

Markets

A brief pause for breath, then onwards and upwards

In the fourth quarter, central banks gave notice that 2024 will see benchmark interest rates falling, driving a strong year-end rally on equity markets. We expect markets to remain within a volatile sideways trend in the first quarter, as the economy performs weakly. An improvement in the economic data accompanied by rate cuts will then take the bull market higher. In regional terms we prefer Swiss equities, in sectoral terms we like healthcare, cyclical and technology stocks. (bae)

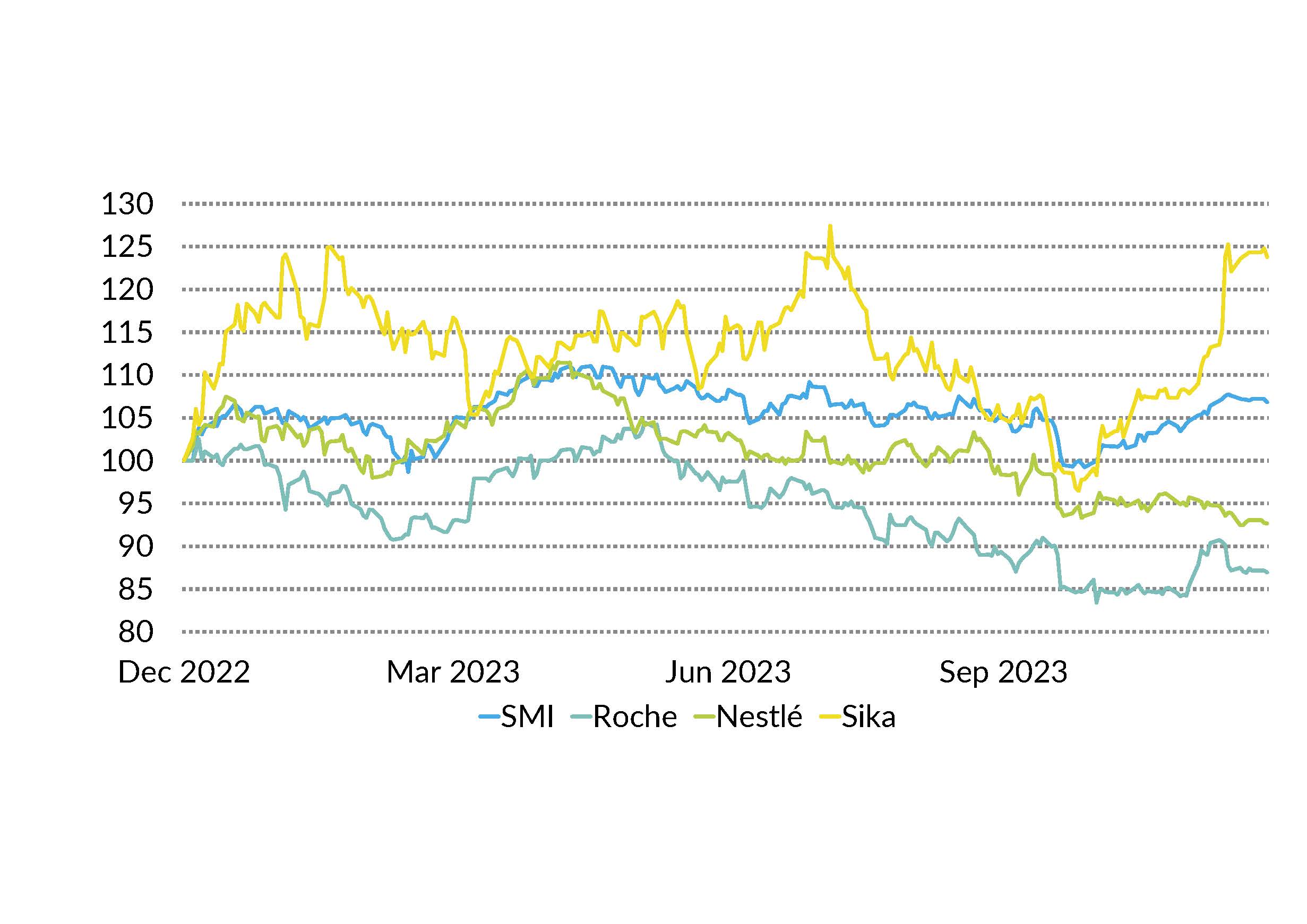

Swiss equities

The Swiss equity market only managed a marginal recovery last year after the heavy losses in 2022 (SPI -16%). This was due to the strong Swiss franc and the disappointing performance of the two index heavyweights Nestlé and Roche. As a result, Switzerland was one of the worst performers among the international equity markets. In our view this suggests considerable upside potential for Swiss equities in 2024. Among blue chips, we favour Roche, Nestlé and Sika; our preferred second-liners are Bachem, SIG Group and Barry Callebaut. (bae)

European equities

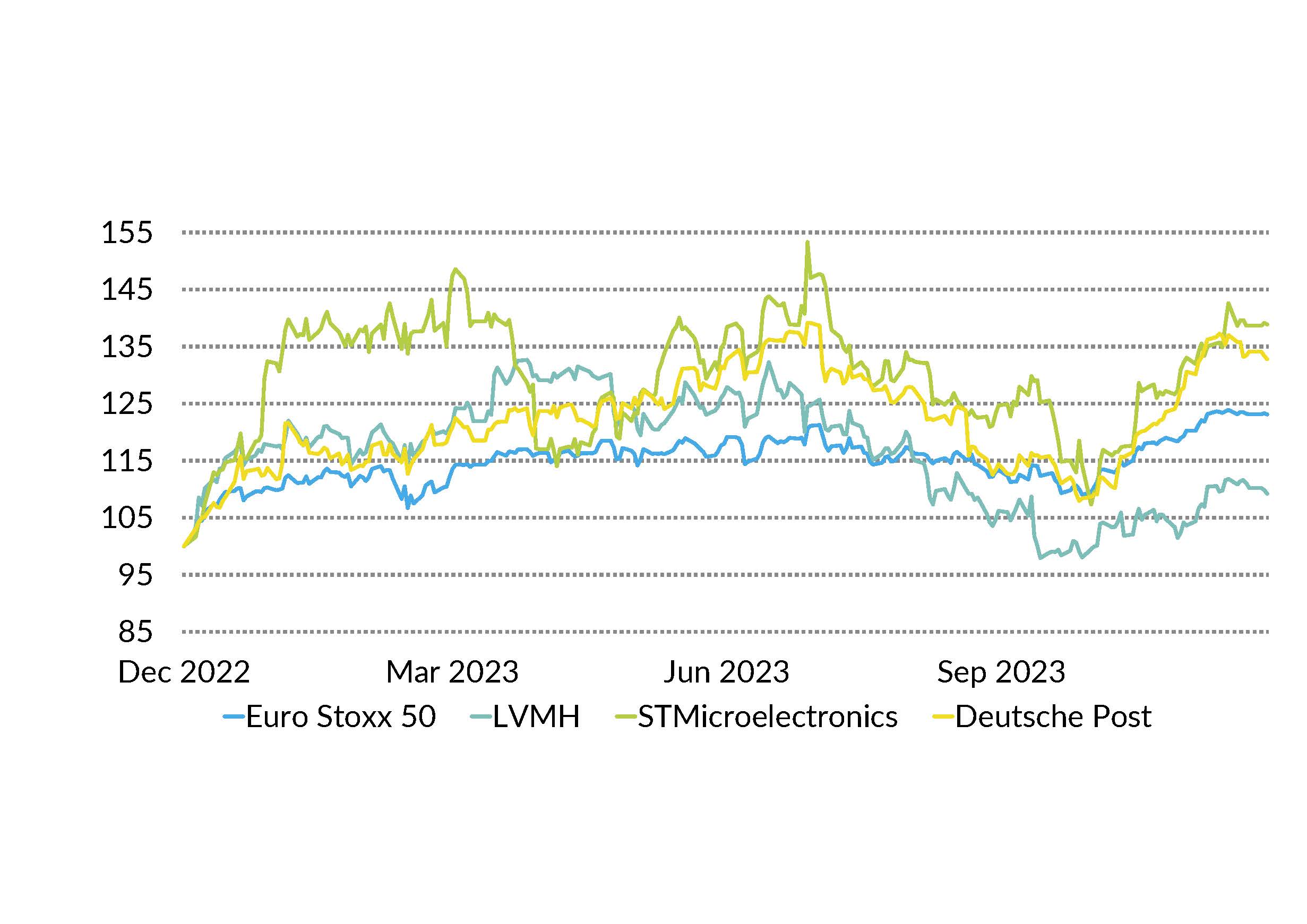

The European equity market, just like its peers, put in a fine performance in the final quarter. However, the threat of a technical recession looms over the continent in the first quarter of 2024. We remain fundamentally positive on the European equity market nevertheless, but feel it will underperform the USA and Switzerland. All eyes will continue to be focused on the ECB. Interest rates, both expected and actual, will keep volatility high and drive the markets. We recommend LVMH, STMicroelectronics and Deutsche Post. (amm)

US equities

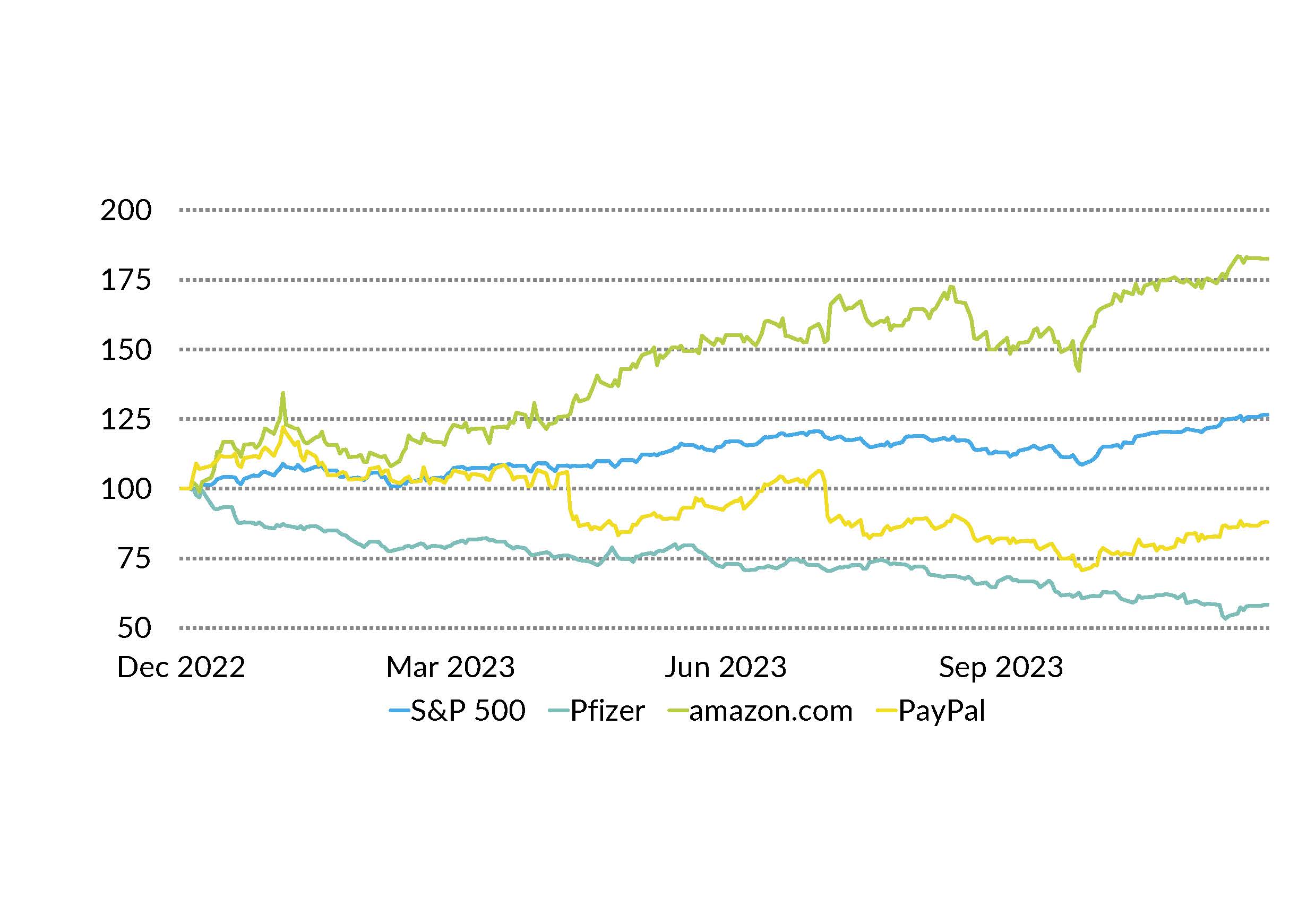

The last quarter of 2023 was a lively time. A weak October was followed by two very strong months that took the S&P 500 back towards its all-time high. We are very bullish for 2024 and expect prices to continue climbing. Things could remain relatively volatile in the first quarter, however, as we do not anticipate interest rate cuts starting until towards the end of Q1 or early in Q2; these will then drive the equity market up sharply once again. We continue to recommend Pfizer, Amazon and PayPal. (amm)

Bonds

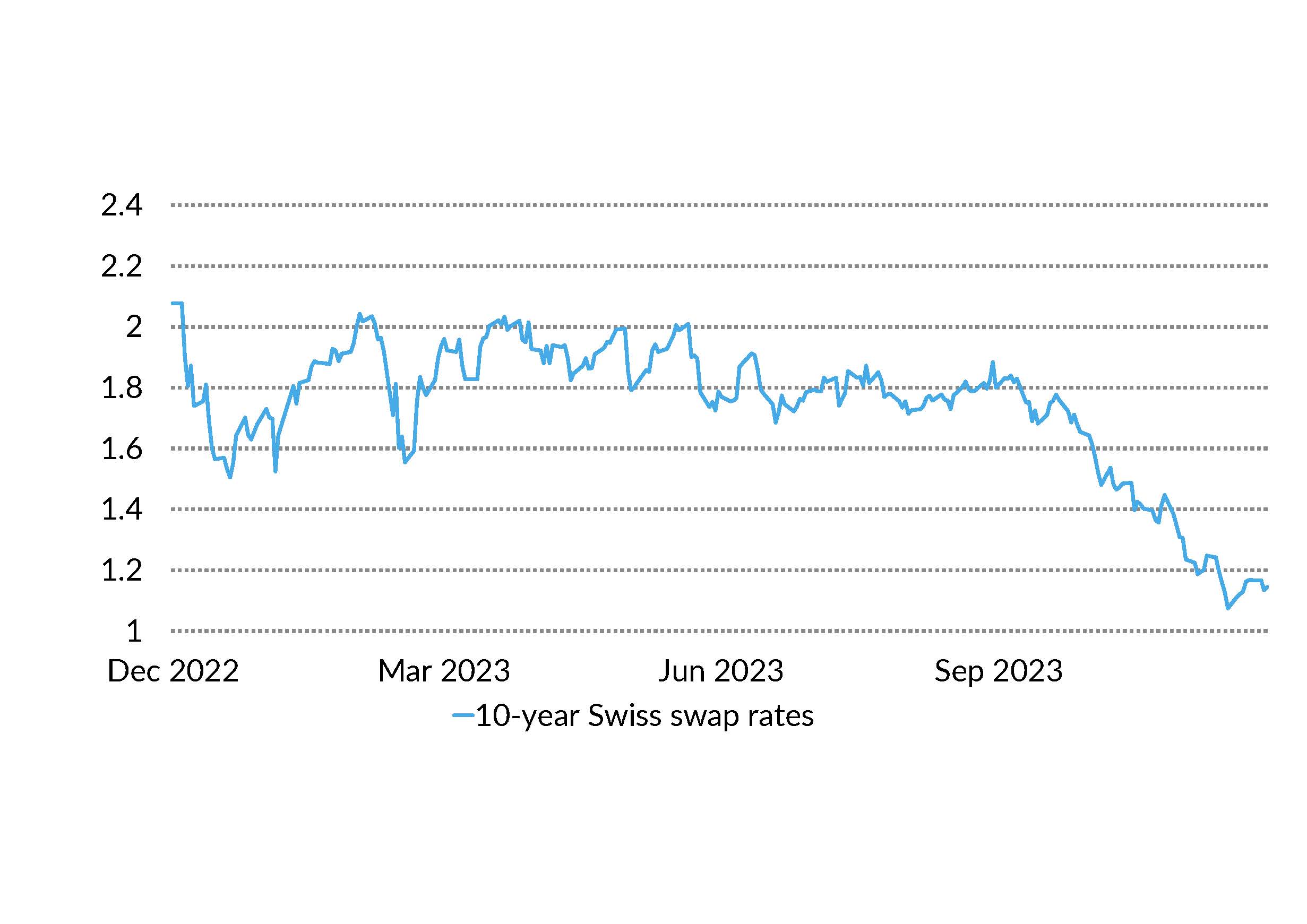

Yields fell significantly in the final quarter as inflation declined more sharply than expected. Markets have begun to price in the definitive end of the tightening cycle and rate cuts in the new year. This has had a positive effect on bond markets. We see potential in sound borrowers rated A-AAA in particular. Our main focus is on bonds in the 1-5 years maturity range, where the expected normalisation of the yield curve could result in major falls in interest rates. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Luca Carrozzo, Sten Götte (goste), Carl Münzer (muc)

Share

Foreword

Luca Carrozzo

CIO