Perspectives 03/2023

Article written on 3 July 2023

The Swiss economy got off to a surprisingly good start to the year, growing by 0.5% quarter on quarter in the first quarter. This was largely driven by domestic demand and capital investment. Annual inflation has been falling steadily in the past few months as a result of energy prices returning to normal, and the situation in the labour market still looks extremely positive.

Time flies – keep an eye on the long term

Time is flying by and the first half of 2023 is already over. After the very negative year on the markets in 2022, the first six months of 2023 restored some calm, with both equities and bonds posting a positive performance.

Even so, investors remain cautious to some extent. Equities certainly went up – by almost 15% in the USA. But a closer look at the performance shows this was dominated by a small number of stocks that benefited from the hype surrounding artificial intelligence. The good performance in Switzerland mainly came from second-liners. That was logical, since these are solid companies that suffered badly last year and are now cheaper.

Investors' caution is understandable; interpreting macroeconomic trends is difficult. Consumer prices are falling, but not as much as desired, and economic growth is well below potential in the various regions. At the same time, labour market reports are remarkably healthy, with very low unemployment rates and large numbers of vacancies.

We are now nearing the end of the cycle of rate hikes by the central banks, so it will be crucial to see how economic growth unfolds. Investors will have to be braced for more volatile times until this reaches a significant level. It is therefore once again important to keep a long-term perspective, even as time flies.

Luca Carrozzo

CIO

Economic prospects

The Swiss economy got off to a surprisingly good start to the year, growing by 0.5% quarter on quarter in the first quarter. This was largely driven by domestic demand and capital investment. Annual inflation has been falling steadily in the past few months as a result of energy prices returning to normal, and the situation in the labour market still looks extremely positive.

Growth below potential

Even so, when it comes to looking at how the economy will fare from hereon in, there's not much to cheer about. The strength of the Swiss franc is keeping a lid on imported inflation, but the recent rise in benchmark mortgage interest rates is likely to push up residential rents. These have a 19% weighting in the consumer price index, so will keep future inflation up.

Weaker growth is the price that has to be paid for using tighter monetary policy to bring inflation back down again. Switzerland is unlikely to be immune to the global economic slowdown. The index of weekly economic activity published by SECO has been under pressure since the end of March. Although leading indicators such as the Purchasing Managers' Index continue to suggest expansion in the services sector, expectations in the manufacturing industry are increasingly heading in the opposite direction, implying a distinct weakening in the industrial sector.

There are no clear signs of where growth will come from at the moment. As a result, economic forecasts for the current year continue to hover around 1%. (muc)

Markets

Bull market in equities facing a test

The cycle of rate hikes by the central banks is coming to an end and inflation is falling owing to the basis effect and the sharp economic slowdown. The impact this will have on corporate earnings remains to be seen. Globally, company profits are expected to stagnate this year. This contrasts with the double-digit rises in share prices seen in the USA and Europe. In the circumstances, we recommend selectively taking profits and adopting a more defensive position in general within portfolios.

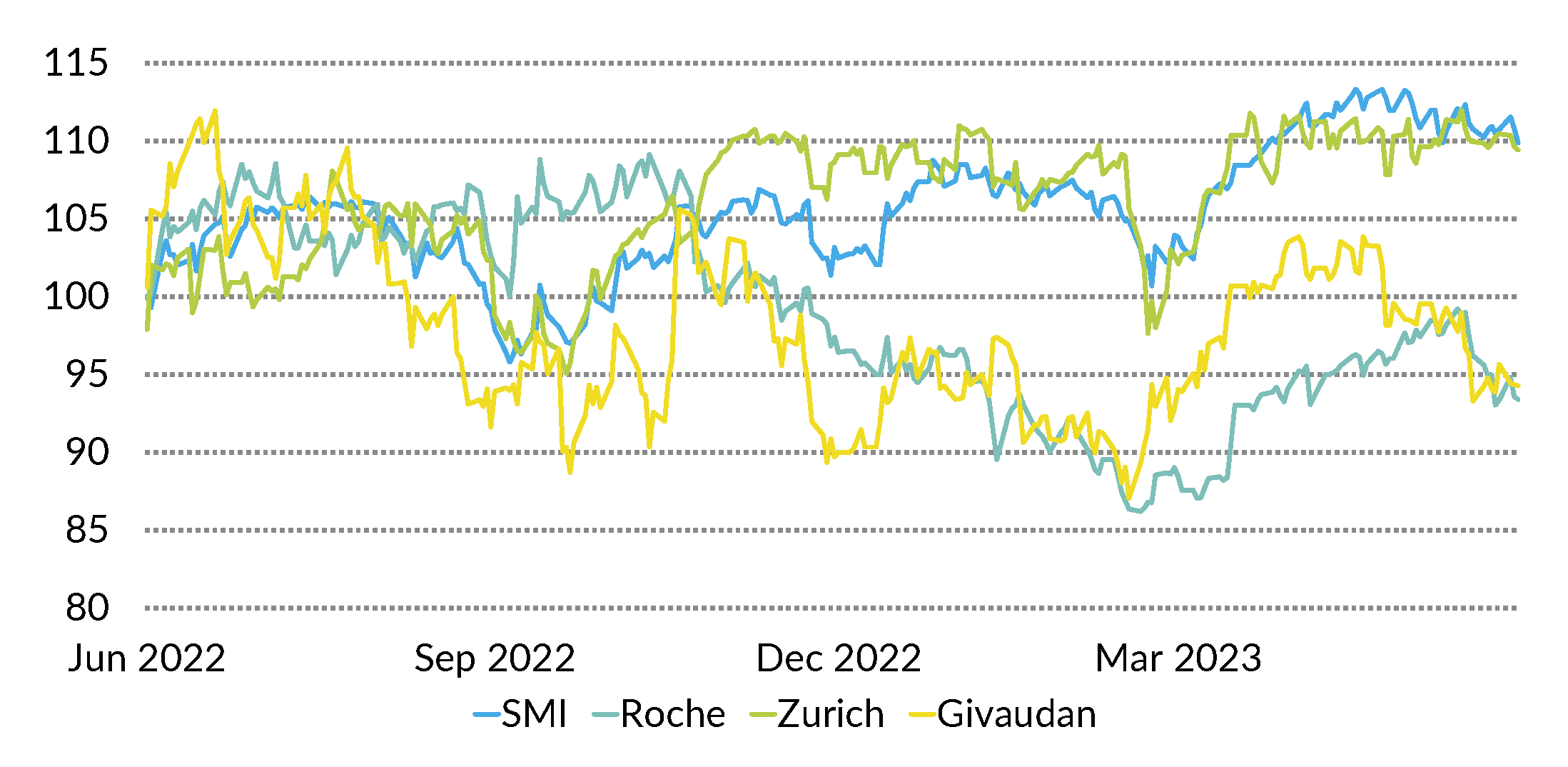

Swiss equities

So far this year, the Swiss equity market has been disappointing because of the poor performance of index heavyweights Nestlé and Roche. Over the summer months, we expect equities to move sideways or slightly downwards, so the Swiss market ought to outperform the USA and Europe because of its high percentage of defensives. Among blue chips, we favour Roche, Zurich Insurance and Givaudan. Our preferred second-liners are Straumann, Swatch and Tecan. (bae)

European equities

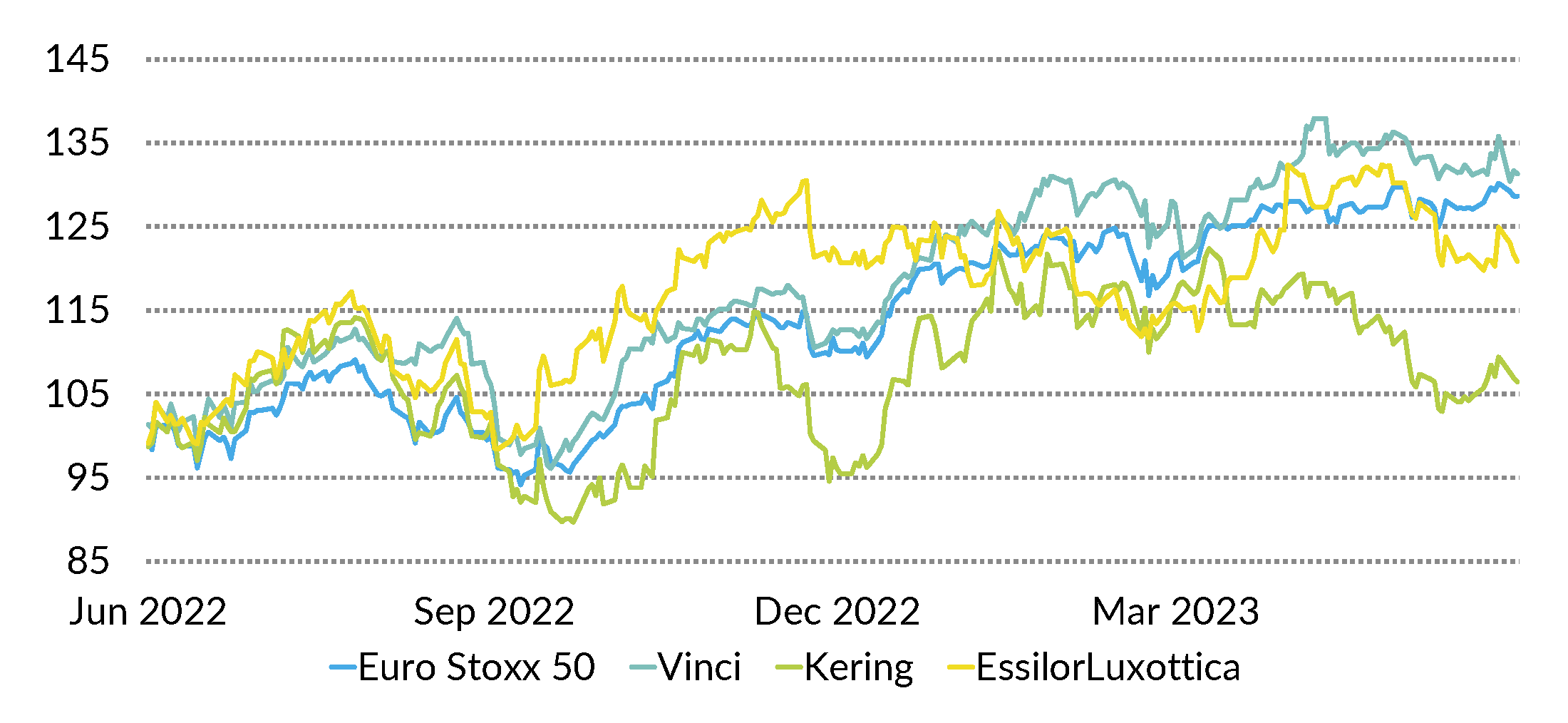

European equities are top of the performance charts this year. Cyclicals like ASML and Infineon, along with Unicredit, stand out and are showing resilience as inflation falls (currently 6.1%, compared to 10.5% in October 2022). The ECB's refinancing rate is 4%, reflecting the longest period of hikes since the central bank for the common currency came into being; this should have an impact on corporate margins. We assume markets will move sideways over the summer and favour EssilorLuxottica, Vinci and Kering. (goste)

US equities

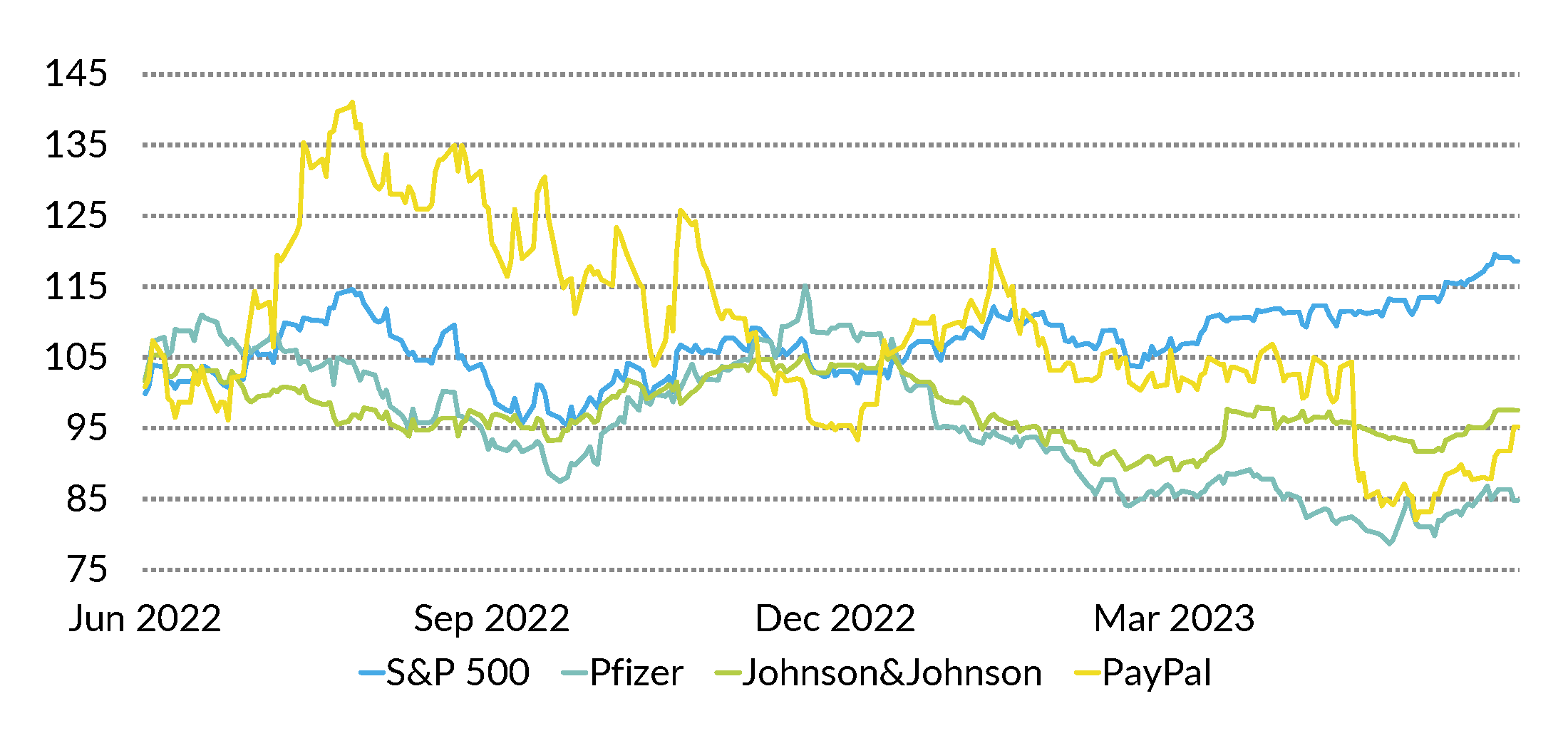

The technology market soared by more than 30% in the first half of the year, driven by euphoria over artificial intelligence. For the current year, though, IT firms see overall profits increasing by less than 1%. Valuations are extremely stretched. In the short term, we expect the market to trend sideways to downwards. The fourth quarter might see the first cuts in interest rates, which would support US equities. We recommend Pfizer, Johnson&Johnson and PayPal. (amm)

Bonds

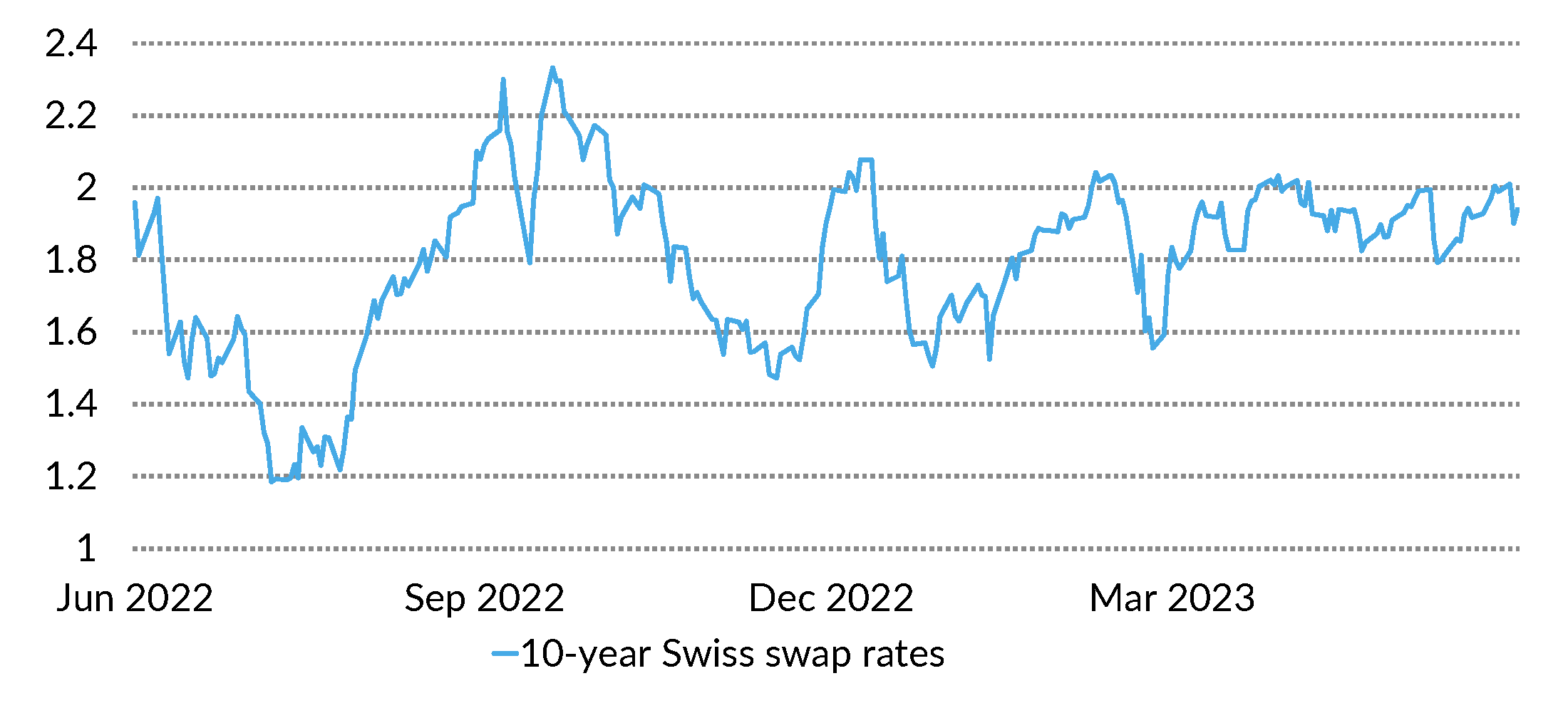

The broad Swiss bond market enjoyed a positive performance over the second quarter. The cycle of central bank rate hikes is gradually drawing to an end and expectations of an imminent loosening of monetary policy have evaporated. The asset class in general is now more attractive thanks to the higher level of interest rates. The Swiss yield curve remains very flat, however, so we favour bonds with a shorter maturity. Owing to the low credit spreads, our focus at the moment is also on quality issues rated A/AA. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Luca Carrozzo, Sten Götte (goste), Carl Münzer (muc)

Foreword

Luca Carrozzo

CIO

Share