perspectives 04/2023

Article written on 2 October 2023

The Swiss economy stagnated in the second quarter. However, the labour market remained strong, which had a positive impact on private consumption. The data published suggest that the Swiss economy is becoming less resilient. The problems encountered by Germany, Switzerland’s largest trading partner, are becoming increasingly evident. Meanwhile, the weakness of China is weighing on industrial exports. This suggests that the slowdown in global growth appears to have reached Switzerland.

Central Banks in a Balancing Act between Inflation and Economic Activity

The regular interest rate decisions taken by central banks were again marked prominently in the calendar this year. Now that the aggressive interest rate hikes appear to be stemming inflation, central banks need to turn their attention to the economy. Slowly but surely, central banks seem to be reaching the end of the cycle of interest rate hikes. When assessing the strategic decisions of central banks, our gold medal for the best central bank in this turbulent year goes to Thomas Jordan and his team. Having surprised market participants in the spring by raising rates before the European Central Bank (ECB), the Swiss National Bank (SNB) now seems to be more in control of inflation than the United States and the European Union. In addition, if you compare the SNB’s communication with that of the Federal Reserve or ECB, the direction of travel is clear. Consumer prices are already within the target range. While economic activity is slowing, Switzerland has not slipped into a recession. In our opinion, consumer prices will remain at the current high level for longer, and Jordan and his team will have more room for manoeuvre if it takes the economy too long to get going again.

Luca Carrozzo

CIO

Economic prospects

The Swiss economy stagnated in the second quarter. However, the labour market remained strong, which had a positive impact on private consumption. The data published suggest that the Swiss economy is becoming less resilient. The problems encountered by Germany, Switzerland’s largest trading partner, are becoming increasingly evident. Meanwhile, the weakness of China is weighing on industrial exports. This suggests that the slowdown in global growth appears to have reached Switzerland.

Purchasing power

The significant hikes in interest rates to fight inflation have begun to have an effect. One example of where this is becoming evident are higher credit costs, which have made business investment and mortgage interest rates more expensive and are partly responsible for growth currently being below average. At the same time, real incomes have turned in a negative performance in recent years. Given that wage growth in Switzerland was already lagging behind inflation in 2021 and 2022 (-0.2% and +0.9% respectively, compared with 1.5% and 2.8%), a further loss of purchasing power this year cannot be ruled out. Considerations of purchasing power are likely to have played a role in the SNB’s surprising decision not to raise interest rates in September. This is because higher interest rates do not just inhibit growth; they also potentially lead to higher rents. In a country where around 58% of the population are tenants, this hits a lot of people in the pocket. However, there appear to be signs that real wages are stabilising. (muc)

Markets

Pause in interest rate hikes supports equity markets

Following a record rise in interest rates in a short space of time, central banks are waiting to see what the impact will be on the real economy. Inflationary pressure is easing as the economy weakens, which is having a positive impact on companies’ profit margins. We consider the risk/return ratio on the markets to be balanced and recommend a neutral equity weighting. However, we would want to consistently take advantage of any larger price corrections to build up quality stocks.

Swiss equities

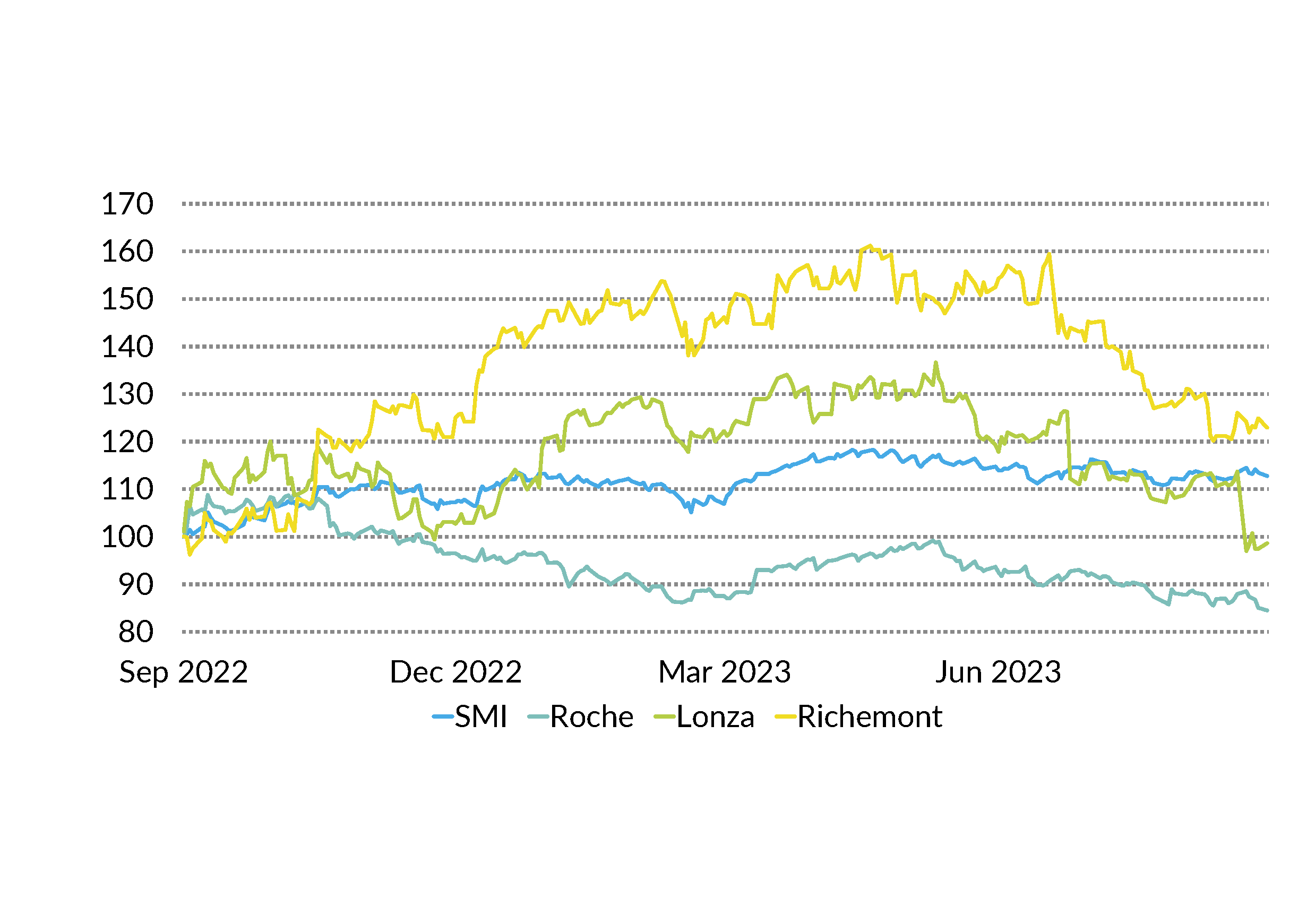

The Swiss equity market is weak compared to other countries owing to the disappointing price performance of the two index heavyweights Roche and Nestlé. Following a decrease of more than 20% in Roche’s share price in 2022, there has been another double-digit decline since the turn of the year. We see significant potential to make up ground here. As a result, the performance of the Swiss equity market is likely to be above average in the fourth quarter. Among blue chips, we favour Roche, Lonza and Richemont; our preferred second-liners are Bachem, SIG Group and Tecan. (bae)

European equities

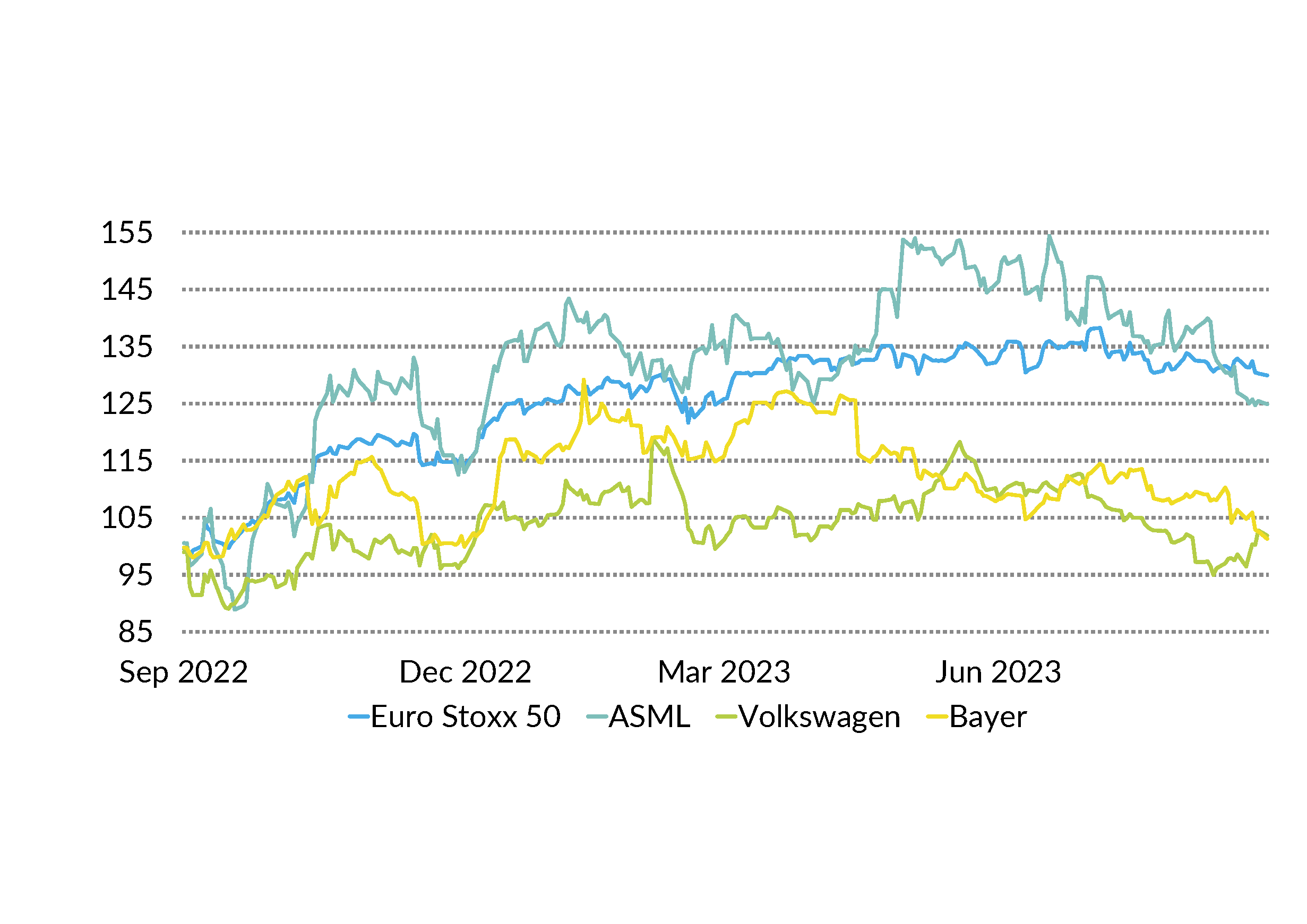

Sentiment is cooling in Europe. France and Germany, formerly linchpins, are currently facing a tricky phase. Recession is in the air. The war in Ukraine is keeping energy prices high, which is putting a strain on the European industrial sector. Against this backdrop, profit disappointments are to be expected, especially with cyclicals. After the high in the Euro Stoxx at the end of July, the market is now losing ground. We are focusing on high-quality stocks and recommend ASML, Volkswagen and Bayer. (amm)

US equities

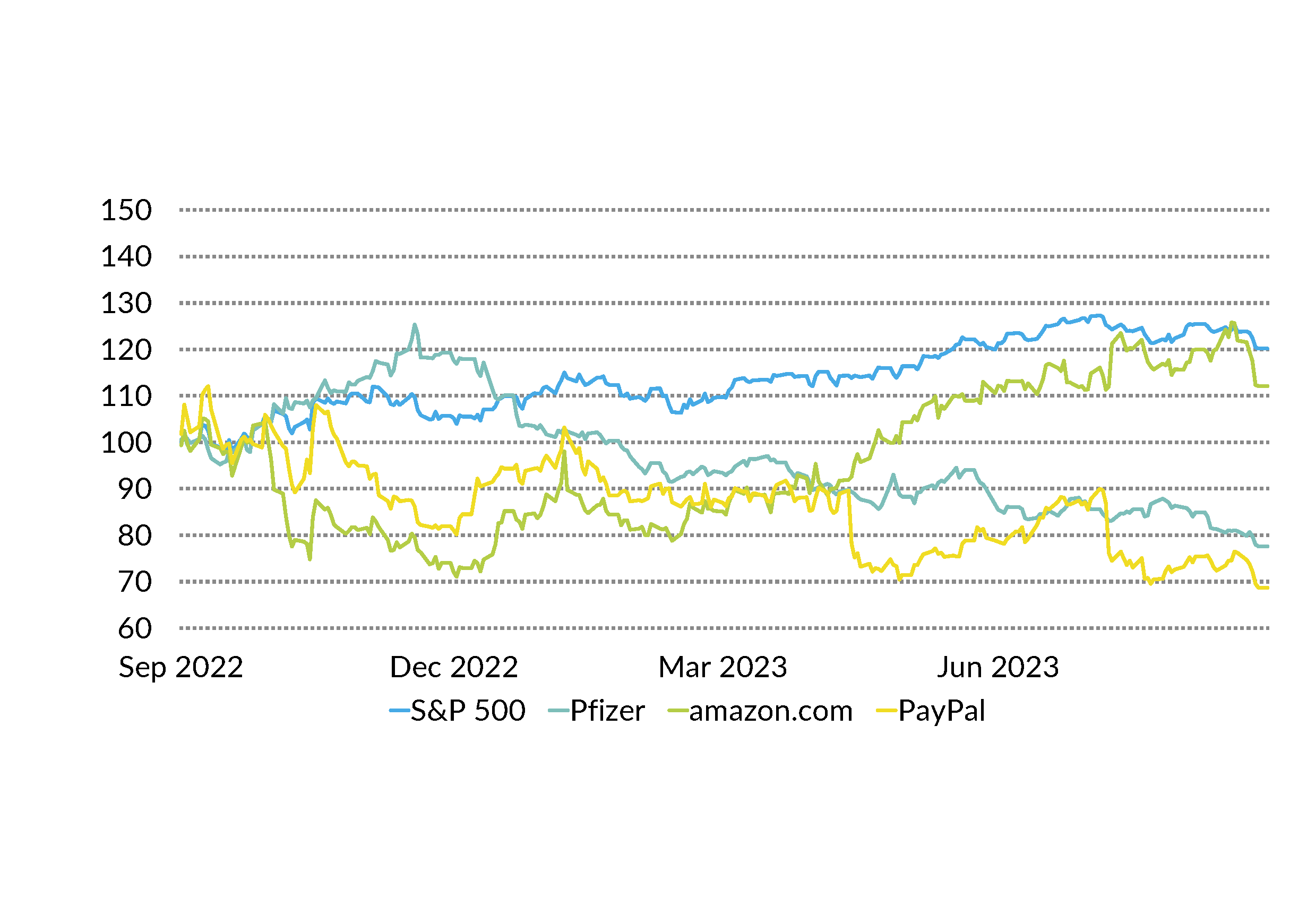

After a tremendous start to the year, the equity market cooled a little in the third quarter. A moderate downward trend dominated the market in the summer months. The high interest rates and the statements made by the Federal Reserve have left the market with virtually no room for rises. We also expect increased volatility for the rest of the year. Despite a strong performance in 2023, the Nasdaq remains below its level at the end of 2021. In the long term, we still believe the technology sector has great potential. We recommend Pfizer, Amazon and PayPal. (amm)

Bonds

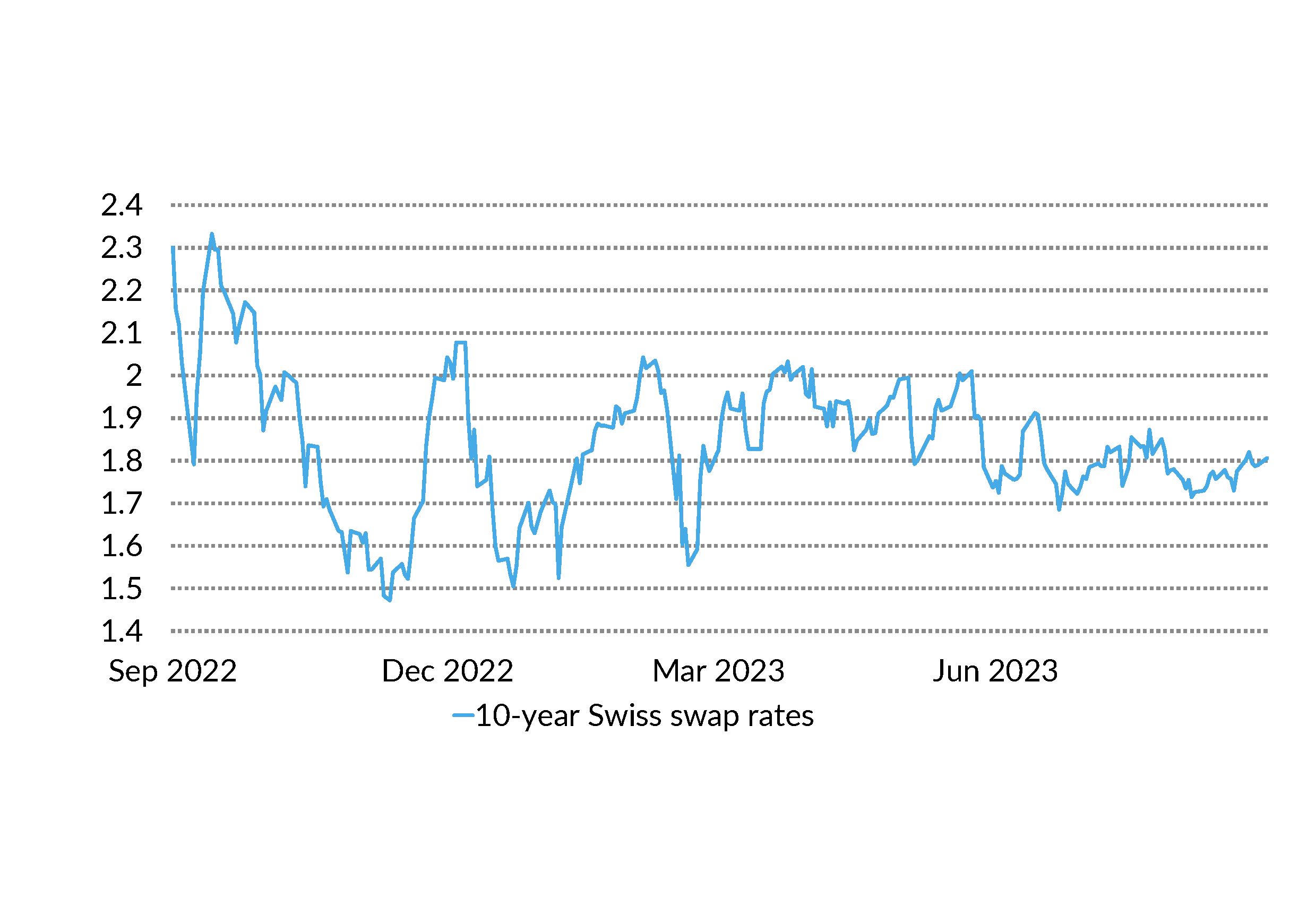

The broad Swiss bond market tended to move sideways over the summer months. Owing to the increasingly tense economic situation, however, the credit spreads on corporate bonds have been widening since the middle of August. The fact that the SNB did not hike interest rates in September led to a considerable fall at the short end of the yield curve. We continue to regard bonds as an attractive asset class and in the current environment favour high-quality securities with shorter maturities rated A/AA. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Luca Carrozzo, Sten Götte (goste), Carl Münzer (muc)

Foreword

Luca Carrozzo

CIO

Share