perspectives 02/2024

Article written on 2 April 2024

The first quarter is already behind us and performance was positive. Artificial intelligence remained a focus of attention and was one of the main drivers of the positive return from financial markets. According to a study published recently, the number of companies mentioning AI in their financial reports has reached a new record: 36%.

Another theme with inflationary tendencies that is moving the markets is the planned rate cuts by central banks. The action they have been taking in recent years appears to have had an effect, as consumer prices have fallen all over the world. But before the relatively high benchmark rates can be cut, Jerome Powell and his colleagues need to be certain that consumer prices will stay low. In the meantime, central banks are happy to wait. Market participants will have to hang on until the summer. In Switzerland, inflation has been within the target range for several months now, so Thomas Jordan has already switched direction to lower the franc. The good news is that rate cuts have a positive impact on the financial market. We have seen in the past that equities tend to go up in the 12 months following the end of a rate hike cycle, as investors expect cuts to stimulate economic growth via rising company revenues and profits. This, plus the warm words from politicians in an election year in the USA, make us positive for equity markets in 2024.

Luca Carrozzo

CIO

Economic prospects

The spectre of inflation had almost become a phenomenon of the previous century, but the changes brought about by the pandemic led to it making a comeback. There are however differences in how fast prices rose. In the eurozone and the USA, they peaked at 10.6% and 9.1% respectively, but in Switzerland at no more than 3.5%. Just under two years after these peaks, significant monetary tightening has slowed the rate of increases substantially.

SNB takes the lead in cutting rates

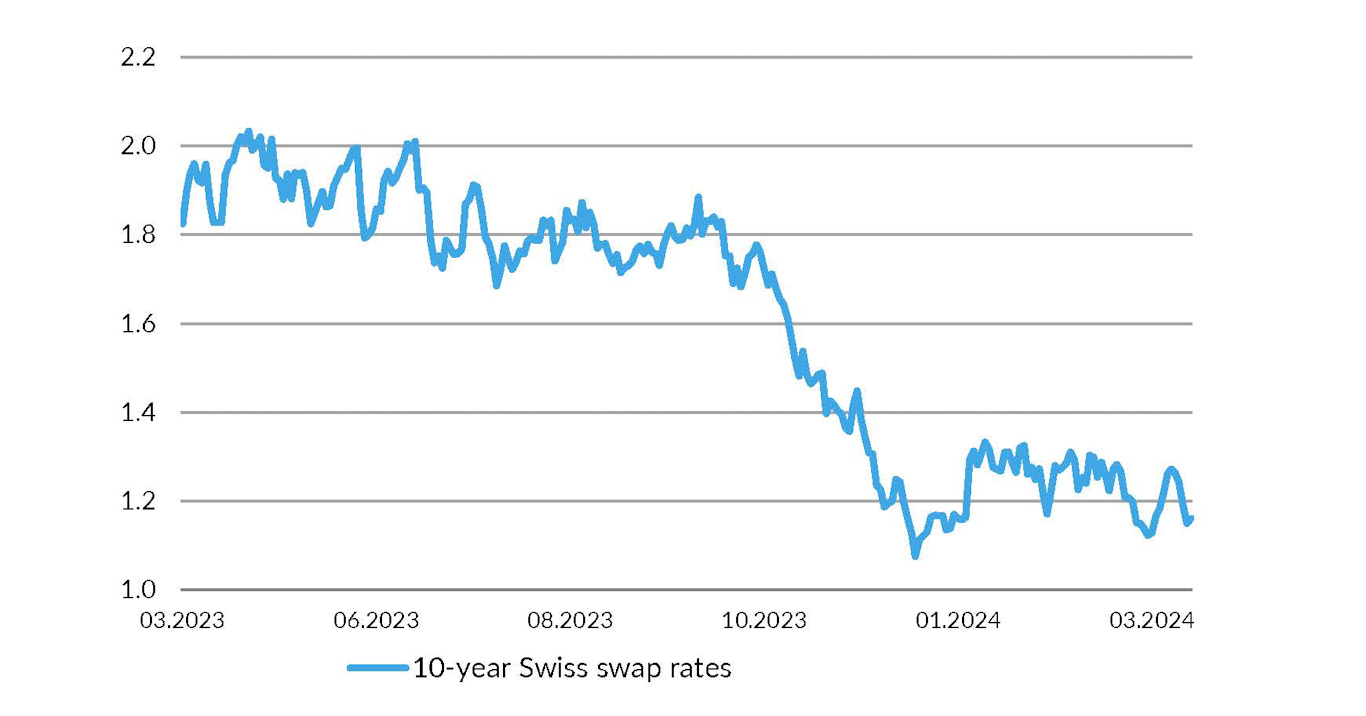

Leading central banks like the European Central Bank and the Federal Reserve are still waiting for the data to improve before cutting rates, but in March the Swiss National Bank surprised the markets by going it alone and cutting rates from 1.75% to 1.5%. This makes it the first major central bank to declare that it has conquered inflation.

In its announcement, the SNB said the more restrictive monetary policy of the past few years had brought price rises back below 2%, the area it deems equivalent to price stability. It also pointed out that the rate cut would support the performance of the Swiss economy. It is forecasting inflation of 1.4% for the current year and, given the prospect of weak foreign demand, subdued economic growth of 1%. (muc)

Markets

Prospect of (further) rate cuts provides support

Stubbornly high inflation rates in Europe and the USA have caused the central banks in those countries to postpone the start of the rate-cutting cycle. But postponed is not the same as cancelled. Inflation in Switzerland is already in its target range, so the Swiss National Bank (SNB) has cut its benchmark rate. The prospect of falling interest rates has pushed some stock markets to new all-time highs. In the second quarter, equity markets will first have to digest these rises, but the traffic lights are still on green. (bae)

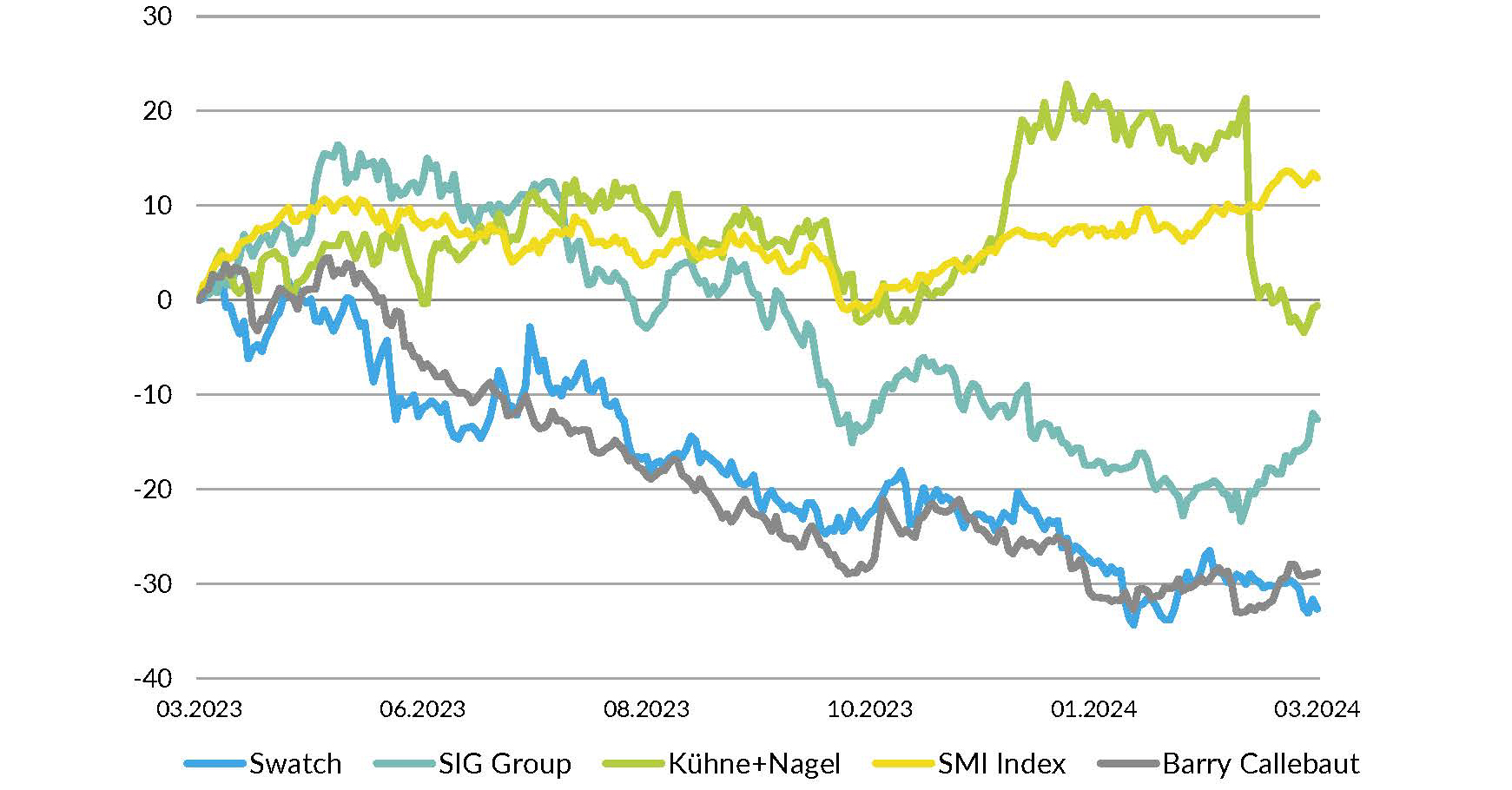

Swiss equities

The Swiss stock market put in a relatively disappointing performance again in the first quarter of 2024. The two index heavyweights Nestlé and Roche are still not getting into their stride and the strength of the franc has had a noticeable impact on first-quarter results. Nevertheless, Switzerland is one of our favourite markets, as the SNB rate cuts are weakening the franc and market participants are far too gloomy about Nestlé and Roche. Among large caps, we also like Kühne+Nagel; in second-liners, SIG Group, Swatch and Barry Callebaut. (bae)

European equities

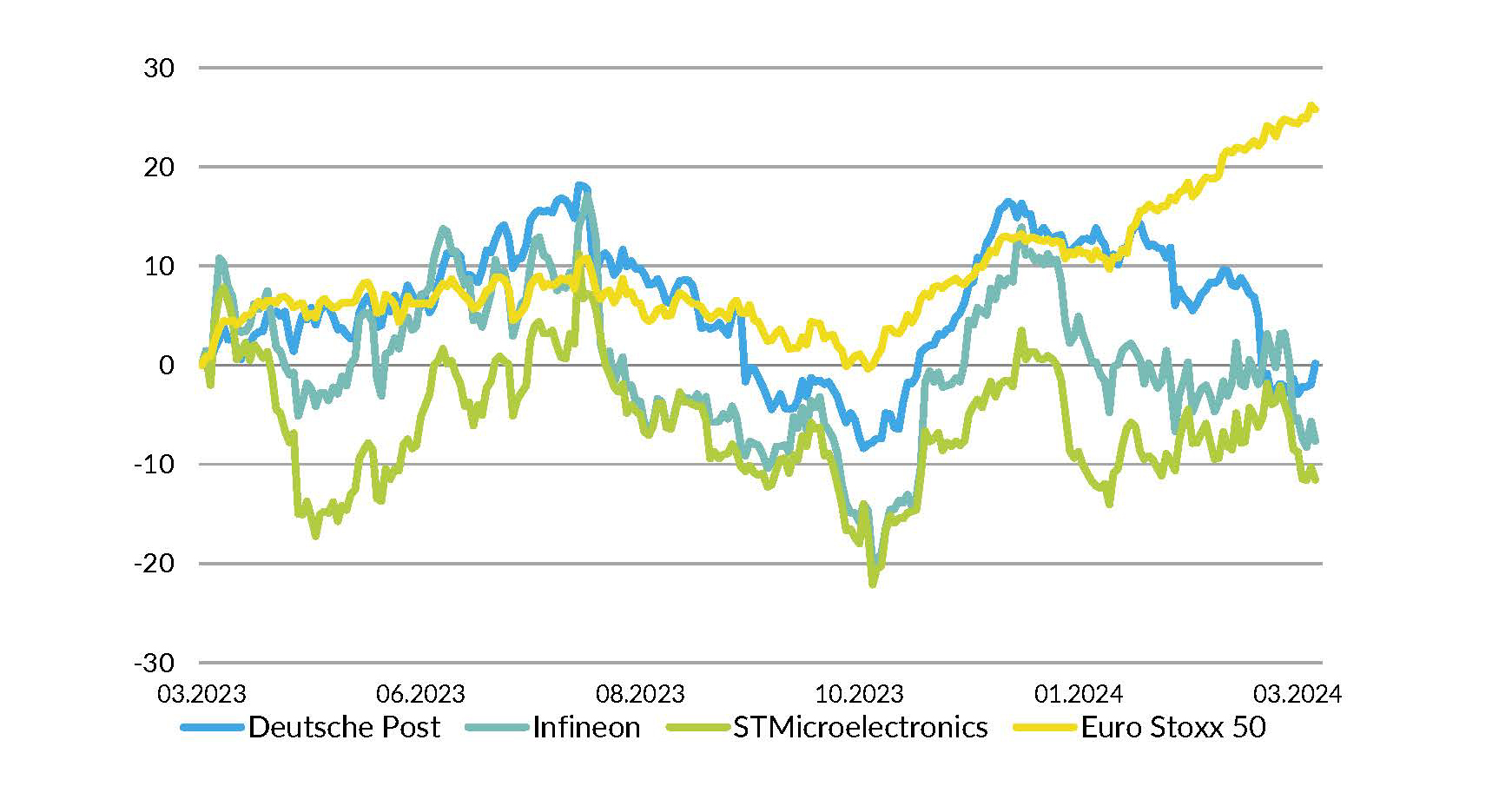

Like its competitors, the European equity market enjoyed a fine leap upwards in the first quarter. The economic data and prospects are not as good as those in the USA or Switzerland, though. Technical recessions in France and Germany are weighing on sentiment. As in the USA, we see a declining market and increased volatility for the time being. We remain positive for 2024 as a whole, however. Our recommendations in Europe are STMicroelectronics, Infineon and Deutsche Post. (amm)

US equities

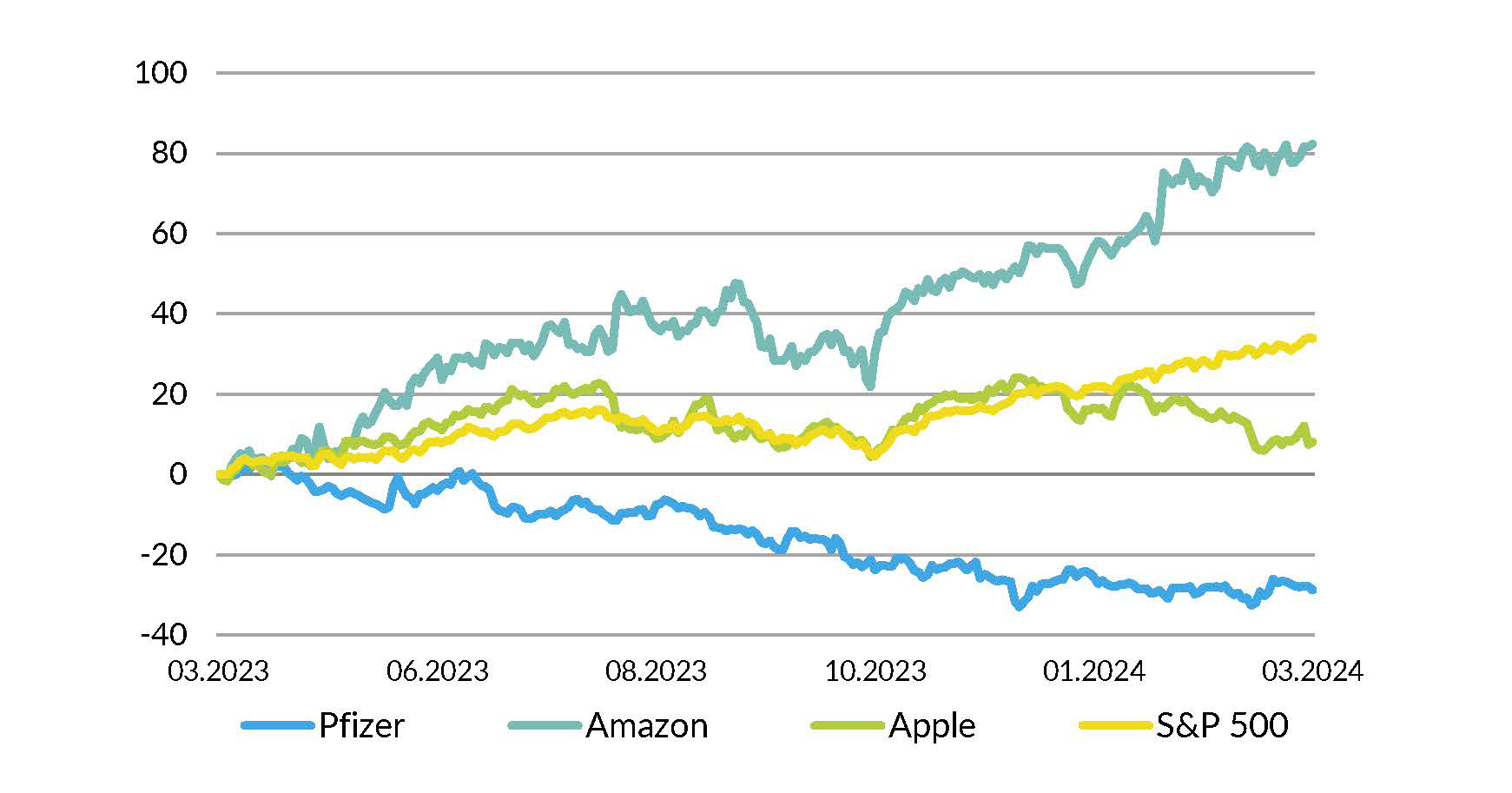

The equity market started the new year with a bang. The S&P500 hit new all-time highs and broke through the 5000 level. The economic data are still too good to allow rate cuts. We do not expect to see the first of the cuts that have been driving markets in recent months until the summer at the earliest. We assume this will take the wind out of the market’s sails. Our expectation is for a volatile market, with potential setbacks for the S&P500 down to 4500. We recommend Pfizer, Amazon and Apple. (amm)

Bonds

Bond markets were unable to find a clear trend in the first quarter. Credit premiums fell slightly in the USA and Europe, but were stable in Switzerland. The only surprise came from the SNB, which cut rates. The reduction in the benchmark rate can be seen as a first step towards normalising the yield curve, which remains inverted. We continue to see the greatest potential in sound borrowers rated A-AAA and are focusing on maturities from 1–5 years. (muc)

Authors:

Marc Ammann (amm), Roger Baumann (bae), Luca Carrozzo (cal), Carl Münzer (muc)

Share