Information on the new SARON® benchmark interest rate

LIBOR (the London Interbank Offered Rate) will be discontinued at the end of 2021. For Swiss francs, LIBOR will be replaced by SARON® (the Swiss Average Rate Overnight). SARON® will be calculated and published daily by SIX Swiss Exchange based on transactions actually executed and prices in the Swiss money market. Please find below more information on the new SARON®.

A brief explanation of SARON®

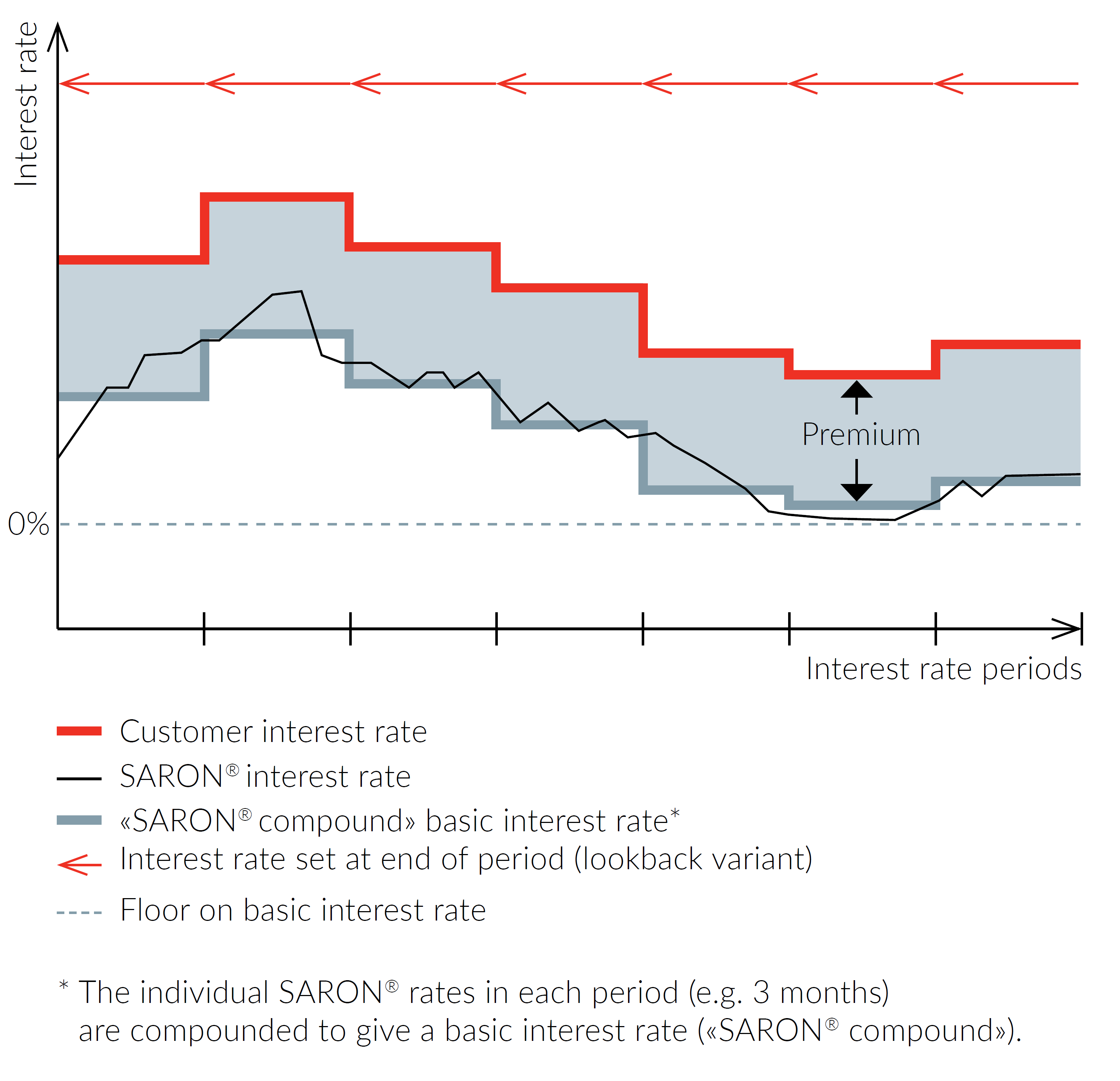

In 2009 the Swiss National Bank (SNB) and SIX Swiss Exchange jointly developed CHF benchmark interest rates for the financial markets. Unlike LIBOR, SARON® is based on actual transactions in the Swiss money market. Interest is calculated using the daily compounded rate (SARON® Compound). This means a change of paradigm in calculation: whereas with LIBOR the interest rate was known at the start of the period, SARON® is not known until the period has ended (lookback variant).

The new SARON® products from Bank CIC

Bank CIC has two products that allow financing using SARON®.

Flex mortgage

The Flex mortgage is a way of financing real estate (residential or commercial) where the interest rate is adjusted regularly every 1, 3 or 6 months in line with the SARON® rate. Interest is calculated using the daily compounded rate (SARON® Compound). The rate is therefore not known until the end of the period. When interest rates are rising, the client can choose to change to another mortgage model at the end of the rollover term.

CIC Flex advance

CIC Flex advance is a medium-term loan for investment, working capital or start-ups. It has a floating interest rate adjusted in line with the SARON® rate every 1, 3 or 6 months. It is calculated using the daily compounded rate (SARON® compound). The interest rate on the CIC Flex advance is set at the start of each agreed interest rate period. This means the rate may be slightly higher than on the Flex advance. The rate remains constant during each of these periods. If interest rates rise the client can switch to another mortgage model at the end of each term.

Frequently asked questions

Expand/collapse all

Why is LIBOR being discontinued?

What is the difference between LIBOR and SARON®?

How is SARON® calculated?

What happens at the end of the interest rate period with a money market mortgage?

Who are the two new successor products suitable for?

What does the switch from LIBOR to SARON® mean for you?